“The secret of freedom lies in educating people, whereas the secret of tyranny is in keeping them ignorant. The king must die so that the country can live.” – Robespierre

Watching with great interest the bloodbath unfolding in the fixed income world thanks to a rapid rise in yields and given our pre-revolutionary mindset we have expressed on numerous occasions in our musings, when it came to choosing our title analogy, we decided to steer once again towards the French Revolution. “Vendémiaire” was the first month in the French Republican calendar which was created during the French Revolution and used by the French government for about 12 years from late 1793 until 1805 and for 18 days again during the Paris Commune French Revolutionary government in 1871. It was meant to replace the Gregorian calendar. The revolutionary calendar was designed to remove all religious and royalist influences from the calendar. It was also part of a larger attempt to decimalization which also included decimal time of day, decimalization of currency and metrication. “Vendémiaire” was the first month of the autumn quarter and started in the day of autumnal equinox. Because it is the season of the vintage in the wine districts it was called “Vendémiaire”. One could opine that central bankers are collecting the “Grapes of Wrath” after years of “financial repression” when it comes to idiotic zero interest rate policies but, we are rambling again.

In this conversation we would like to look at the implications of the significant rise in yields as well as the current weakening of the macro picture and what it entails.

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Synopsis:

Yields of wrath

The fall in the fall?

· Yields of wrath

We are seeing a rapid acceleration in rising yields on a global scale and as such the wheels are starting to come off the proverbial cart with the return of the “bond vigilantes”:

- Graph source Macronomics - KOYFIN

Convexity is starting to bite on the long end of US Investment Grade credit which is not really a surprise duration exposure wise:

- Graph source Macronomics

We are close to seeing some very enticing entry points from a carry and roll-down perspective:

- Graph source Bloomberg – Twitter/X

Yet credit risk wise 5 years CDS spreads are still well behaving YTD:

- Graph source Macronomics – Datagrapple.com

Cracks are yet to show up in the credit space and the performance of the credit canary CCCs rated US High Yield has been so far stellar in 2023 (Energy exposure related mostly):

- Graph source Macronomics – KOYFIN

Even in Emerging Markets, one would have expected that the relentless rise in US Treasuries yields would have crashed the Emerging Markets Fixed Income party à la 2013 taper tantrum but it is not the case:

- Graph source Macronomics – KOYFIN

It appears to us that in credit land CFOs have been much more apt in managing their refinancing needs, maturity wall and duration exposure relative to the Fed.

On a side note we remain very puzzled to this day on why the Fed did not re issue its 50 years long bond and extended its duration:

- Graph source Bloomberg – Twitter/X

From our twitter feed we totally agree with “Credit from Macro to Micro aka @Credit_Junk:

“As said before term premium was driven lower by low inflation, fiscal surpluses, etc, etc. Now all drivers reversed and term premium returned positive. This is negative for belly of the curve (10y underperforming) due to uncertainty. You need real assets in this environment.”

“We are in the age of Fiscal Dominance. Credit spreads are well behaved CDS wise so it is all about "bond vigilantes"” – Macronomics - Twitter

As a reminder from our previous conversation:

“The US fiscal trajectory is unsustainable because of Quasi Fiscal Deficit in the US. (For more on QFD issues we highly recommend watching Geoffrey Fouvry quick take on Graph Financials, part 1 and part 2). US Treasuries seems to be more and more trading like Emerging Market bonds when it comes to “volatility”.

Some financial pundit has been pointing out towards China shedding US Treasuries for the rise in US long yields given China has cut its holdings in US Treasuries to $822bn, lowest level since 2009. Beijing has been selling $300bn in Treasuries since 2021, and the pace of Chinese selling has been faster in recent months, Apollos's Slok has calculated:

Of course we promptly asked Holger on Twitter / X if China is to be blamed for “Fiscal Dominance” and the US budget deficit trajectory:

- Graph source Bloomberg – Twitter/X

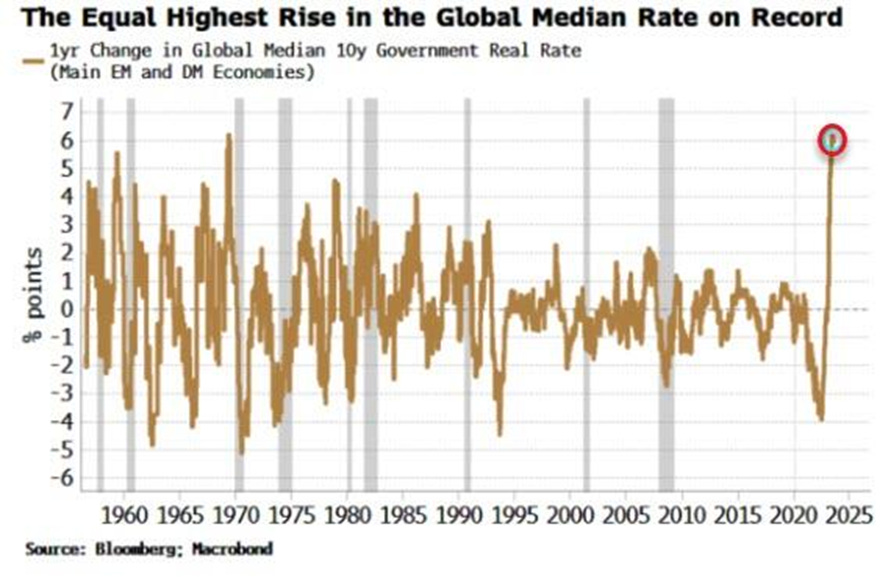

“Bond vigilantes” we think are smelling blood and as such are on a “Vendémiaire” rampage hence our “Yields of Wrath” subtitle and pre-revolutionary mindset in our “musings”:

- Graph source LSEG Datastream – Twitter/X

And the “Yields of Wrath” have so far been rising significantly and at a very rapid pace:

- Graph source Bloomberg – Twitter/X

In our last musing we pointed out to “Monetary regime change” which, we think is a manifestation of BRICS+ and somewhat dollar “rebellion” against the US dollar “Empire”.

As per our August conversation this is what we had to say:

“The weakening of the Japanese yield is the consequence of significant amount of bonds purchase by the Bank of Japan. As we pointed out in our March conversation “The Cheshire Cat”, Japan already owned 56% of the Japanese government bond market and given their willingness in boosting their defense spending and that Japanese are reluctant to accept tax hikes, the easiest way of course is therefore to issue more bonds and for the Bank of Japan to buy more of it.” – Macronomics, August 2023

We have highlighted on numerous occasions that there has been a significant weakening of the Japanese yen in synch with the rise in US Treasury 10 year yields (6 months chart):

- Graph source Macronomics – TradingView

Of course, what is happening is what we predicted namely that the Bank of Japan announced on the 29th of September an unscheduled bond-purchase operation overnight to dampen the selloff in the nation's debt. It was only $2 billion worth of purchases and so far didn't really scared the ”bond vigilantes” and left rates on 30-year notes at the highest in nearly a decade and inflicting significant losses in the process:

Graph source Bloomberg – Twitter/X

The Bank of Japan will try to do more of the same:

“The Bank of Japan is planning another bond-buying operation. But “the additional operations could accelerate the speed of the yen’s weakening” by preventing debt yields from rising. “It will eventually become impossible to continue with these operations” “ - Bloomberg

We don’t think it will be “enough” to tame the bonds revolutionaries during the period of “Vendémiaire”.

· The fall in the fall?

We have noticed a clear deterioration in European PMIs and as well our own country France based its latest 2024 budget on a “phoney” annual growth assumption of 1.4% and is also looking at issuing 285 billion Euros of debt in 2024, a new record:

“Eurozone manufacturers continued to report a sharp contraction in September, the HCOB economics PMI signalled (43.4), as new orders shrank at one of the fastest rates since the survey began in 1997."

- Graph source S&P Global PMI

US Treasuries seems to be more and more trading like Emerging Market bonds when it comes to “volatility” (MOVE index VS VIX index, one year chart):

- Graph source Macronomics - TradingView

In our previous conversation we mentioned that there was a monetary message coming from “soft commodities” with Cattle Futures closing at an all-time high again in conjunction with Orange Juice and Sugar. As well we reiterated what was in our February conversation “Tantalean Punishment” that back in 1933 a group of young investors in Boston started to worry about inflation and how it would affect bonds and stocks value and after two years of study they set up the first commodity investment trust in the world called Commodity Corp. in 1935.

On top of the return of the “bond vigilantes” we think that commodities are getting somewhat “unglued” when we read that Nigeria has set October BONNY crude official selling price to plus 291 cents/bbl versus dated Brent! Things are getting interesting and not only when it comes to “arbitrage” between gold prices set up in Shanghai versus gold prices set up in the West. China-Brazil have also implemented yuan denominated, settled and financed transactions therefore bypassing settlements, and financing in US dollar, in effect neutering imported inflation from the US.

Please remember the work of Professor Edwin Walter Kemmerer he was a professor of economics at Princeton University. He became famous as a "money doctor" or economic adviser to foreign governments all around the world, promoting plans based on strong currencies and balanced budgets. He also helped in the design of the US Federal Reserve System in 1911:

“A price is the value of a particular commodity in terms of the value of the monetary unit. It is an expression of the number of units of money for which a commodity is bought and sold. The price level represents a composite of individual prices. Prices fluctuate, therefore, with the changing value of goods and also with the changing value of money.” – Edwin Walter Kemmerer – The Prospect of Rising Prices from the Monetary Angle

If the only satisfactory hedge against inflation is commodities as thought by investors in 1933, we are not surprised to a continuation of the rally in soft commodities in particular. Since it’s low in 2020, the price of orange juice is up 270%. This year alone, orange juice prices are up 70%:

- Graph source The Kobeissi Letter – Twitter/X

Rising yields is also leading to rapid tightening of financial conditions and as we indicated on numerous occasions we are not buying the “soft landing” narrative in terms of the latest Jedi Tricks of the sorcerer’s apprentices at the Fed (in similar fashion we did not buy the inflation is transitory narrative):

"The most likely outcome is that the economy will move forward toward a soft landing." Janet Yellen said this in October 2007, two months before the start of the Great Recession.

The number of banks tightening lending standards has reached one of the highest levels in the last 35 years and has usually foreshadowed a recession:

- Graph source Bloomberg – Twitter/X

The number of small businesses filing for bankruptcy is surging:

- Graph source Barchart – Twitter/X

Facts:

Firms with less than 20 employees make up 90% of all companies in the US

Small and medium-sized firms employ half of all workers in the US

Small and medium-sized firms generate half of all revenue in corporate America

Small firms create around 3mn jobs every year

We are also seeing the start of a significant widening in US Financials CDS which clearly indicates to us an indication of the deterioration of the macro environment:

- Graph source Joe Consorti Bloomberg - Twitter/X

In our August conversation “Fortune cookie” we made an “interesting comparison” just for the fun of the argument, where we argued that JP Morgan Senior CDS at 55bps was trading too tight relative to China (84 bps in August) given the most recent S&P multiple US Banks downgrades on growing liquidity worries as well as Fitch downgrading the United States of America’s rating. Now China 5 year CDS is trading around 82 bps, 2 bps tighter whereas JP Morgan 5 year CDS is trading at 66 bps, 11 bps wider. Maybe we were somewhat right after all but we digress.

- Graph source Macronomics - Datagrapple.com

So much for the China “Lehman” moment touted by many financial pundits.

When it comes to the “fall in the fall” during the Vendémiaire season, in our book a “Bear steepening” is not favorable to “risky assets”. US 10 year vs 3 months:

- Graph source Macronomics - KOYFIN

Bear steepening commonly occurs when investors are concerned about inflation. With the term premium returning “positive”, you have all the red flags you need thanks to the “Yields of Wrath”:

- Graph source Bloomberg – Twitter/X

13 Vendémiaire, in Year 4 in the French Republican Calendar (5 October 1795 in the Gregorian calendar), was the name given to a battle between the French Revolutionary troops and Royalist forces in the streets of Paris and it was a major factor in the rapid advancement of Republican General Napoleon Bonaparte's career but that’s another story. It also marked the end of the French Revolution. We have yet to see the end of the “bond revolution” so we think you should buckle up.

With Geoffrey’s help, we endeavor to touch more on various subjects through GRAPHFINANCIALS

Geoffrey’s view point is that we probably have a bull trap for the USD vs commodities. Typically long bond yields rise if it comes from a demand from private credit meaning higher profits expectations. However with Manufacturing PMI at 49.8 this is not the case. We have to discard the possibility that the rise in long bonds is coming from the credit part of the US dollar. On the other hand, we have a massive supply from the fiscal part of the currency that is: a large supply of Government bonds hitting the markets. In the first case the rise in the long bond is bullish for the US dollar versus the commodities, but, in the second case it is bearish for the US dollar versus the commodities and that’s where we are we think.

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so. “ – Mark Twain

You can join Macronomics on our Telegram Channel indicated in our Twitter profile as well you can join our Twitter feed. Going forward we will publish more frequently on our dedicated Substack page.

PERSONAL COMMENTS ON MACRO TRENDS, MACRO NEWS AND VIEWS. ALL RIGHTS RESERVED. DISCLAIMER: INFORMATION PROVIDED ON THIS BLOG DOES NOT CONSTITUTE A RECOMMENDATION OR ADVICE TO PURCHASE ANY INVESTMENT, PRODUCT OR SERVICE LISTED OR MENTIONED ON THIS BLOG. INFORMATION DISPLAYED ON THIS BLOG IS NOT INTENDED AS SPECIFIC INVESTMENT ADVICE AND SHOULD NOT BE RELIED ON FOR MAKING INVESTMENT DECISIONS.

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Martin - again Eclairant, you never cease to amaze Mon Ami.