Looking at the change in the inflation narrative leading to the “higher for longer” scenario as we posited in our last conversation, when it came to selecting our title narrative we decided once more to steer towards a Lewis Carroll title analogy. The Cheshire Cat is a fictional cat not only known for its distinctive mischievous grin but also for the philosophical points he raises that annoy of baffle Alice in Lewis Carroll’s book. The Cheshire Cat in similar fashion to the US Fed takes a pleasure, it seems at “misdirecting”. As well, in science, the Cheshire Cat effect as described by Sally Duensing and Bob Miller is a binocular rivalry which causes stationary objects seen in one eye to disappear from view when an object in motion crosses in front of the other eye. Given that each eye sees two different views of the world, those images are sent to the visual cortex where they are combined and create a three-dimensional image. The Cheshire Cat effect occurs when one eye is fixated on a stationary object, while the other notices something moving. Since one eye is seeing a moving object, the brain will focus on it, causing parts of the stationary object to fade away from vision entirely. While financial pundits eyes are focusing on the inflation as a moving object, what seems to be fading away from the vison of these financial pundits are the deterioration of segments of the credit markets where we are already seeing significant impairments in the commercial real estate space with the occurrence of “strategic defaults” and also slowing “credit growth”. You already know by now that like the Cheshire Cat engages Alice sometimes in amusing “perplexing conversations”, we enjoy doing the same dear readers.

In this conversation, we would like to continue to discuss the inflation issues weighting on central banks action in general and the ECB in particular as well as the issues facing both the government of Japan and the Bank of Japan.

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

· The Cheshire Cat effect

Looking at the latest raft of macro releases in Europe from stubborn inflation to weakening PMIs, in the central banking world, it seems to us that the ECB is indeed more in a bind than its counterpart the US Fed. With Core European inflation running at 5.6%, the ECB is facing an uphill struggle:

“ECB terminal rate rises 60bps in a month, jumping above 4%. Euro-Area inflation print on deck today, focus on the core reading. The country prints have all come in above expectations this week:

Germany 9.3% vs 9.0% exp.

France 7.2% vs 7.0% exp.

Spain 6.1% vs 5.7% exp.” – Valerie Tytel – Bloomberg

On top of inflation woes, European Government bond yields have been rising in conjunction with central banks hiking activity:

- Graph source Macronomics – KOYFIN

German bonds also have been trending higher yield wise across the curve with 2 years, 5 years and 10 years rising by 20bps in three sessions:

- Graph source Bloomberg

On top of that ECB is starting its “Passive QT” meaning a reduction of €15bn per month in March until June. It will be a passive roll-off from APP facility only, not PEPP. Currently ECB assets equate to €9T, of which government bonds represent €5T. Markets did absorb an effective net debt supply of €280bn in 2022, but with QT 2023's it balloons to +€600bn!:

- Graph source Bloomberg

While high inflation is somewhat “eroding” the debt value, when it comes to French cost of debt we are concerned by the size of linkers (OATi) and the rising cost in terms of interest payout. As we pointed out last year in our twitter feed, 2022 cost of debt in France rose by €17 billion including €15 billion for OATi which are tied to inflation. France issued big amounts in early 2022. What were they thinking ?

France has historically pioneered inflation-indexed sovereign bonds as the first euro-area country to issue one in 1998 and has continued to issue them on a regular basis. Should inflation exceed expectations and persist longer run, France could be among the euro-area countries for which debt service increases the most as consequence of such higher-for-longer inflation. Inflation-linked debt amounts to around EUR 246bn, about 11.3% of outstanding debt. There is a mounting risk that the increase in OAT€i bond payments outpaces that of fiscal revenue and further increases an aggregate cost of public debt. Just saying…

As we pointed out in our recent conversation ”State of Ambivalence”, once the "Inflation Genie" is "Out of the Bottle" as warned by Fed's Bullard in 2012, it is hard to get it back under control:

“There’s some risk that you lock in this policy for too long a period,” he stated. ”Once inflation gets out of control, it takes a long, long time to fix it” - Bullard

In our last conversation we hinted again on our “pre-revolutionary” mindset which has been displayed on numerous occasions in our musings during many years. In 2016 on our blog, we used a reference to the French revolution with the term “Thermidor” for our title analogy. The French Republican Calendar was implemented during the French revolution and used by the French government for about 12 years from late 1793 until 1805, with Thermidor (or Fervidor) starting the 19th or 20th of July and coming from the Greek "thermon" meaning "summer heat". On many printed calendars of Year II (1793–94), the month of Thermidor was named Fervidor (from Latin fervens, "hot"). In 2016, France was about to harvest the least wheat in 28 years. We also pointed out in our last conversation that the proper French revolutionary period (1789-1794) was characterized by poor harvests and very similar meteorological factors witnessed in 1788 and 1789, namely very hot spring-summer periods with very bad weather followed by very cold winters (-21 degrees Celsius in Paris during the winter of 1788) as a reminder. It happens that we just learned that France has gone through a record 32 consecutive days without rain, the longest streak since 1959. No wonder we continue having this “pre-revolutionary thoughts” we think but like a Cheshire Cat, we are wandering again in our labyrinth of thoughts:

- Graph source Bloomberg

Returning to the “fervidor” subject of entrenched inflation, the ECB is much more “behind the curve” than the US Fed, thanks to energy woes and rising core inflation. Given the current inflation headache for the ECB, they will have to be more restrictive and as such they will have to hike in that context which will no doubt put downward pressure on the already fragile European economy, no “soft landing” there but most likely “recession” given we are seeing in Europe rising bankruptcies:

- Graph source Eurostat

In the current context of rates differential between the US and Europe, what caught our attention (H/T Alex Goncalves), is our gold price performance has been tracking very closely the performance of EUR/USD for a year:

- Graph source Macronomics – Refinitiv Eikon

Our long-time followers know that we have been fearful of a materialization of “stagflation” unfolding. Another validation came recently from the “wise sorcerers” of the BIS in their most recent quarterly report where they pointed out the following:

“Over the past few years, commodity prices and the US dollar have moved in tandem, a departure from the historical pattern with stark implications for stagflation risk”

- Graph source BIS

The BIS concluded this particular study with the following:

“The role of commodity prices and the dollar as risk factors was very apparent during 2021/22. In the wake of the Russia-Ukraine war, commodity prices rose steeply, and the US dollar appreciated, before both trends reversed in late 2022. The joint surge in commodity prices and the dollar was associated with a steep rise in inflation and a marked slowdown in economic growth globally during 2022. Our analysis suggests that the individual stagflationary effects of commodity prices and the dollar on commodity-importing economies have compounded each other over this period as the two variables increased in tandem. This was a break from the historical pattern, when commodity prices and dollar used to move in opposite directions, so that their individual effects on stagflation risk tended to offset each other.

A lasting positive correlation between commodity prices and dollar exchange rate would imply greater challenges for macro-financial stability policies going forward. It could lead to greater macroeconomic volatility and more difficult trade-offs between inflation and output stabilisation.” – Source BIS

The Fed has two stark choices, either crash the economy or crash the dollar. For now renewed inflationary pressure as we pointed out in our previous conversation is forcing the Fed to pivot the other way, hiking for longer that is.

· Watch the Bank of Japan very closely

In similar fashion 2022 was marked by a strong relationship between the US 10 year yield and the Japanese yen:

- Graph source Macronomics – Refinitiv Eikon

We find of interest the growing gap between the USTs 10 years yield firmly above 4% (4.08) and the Japanese yen, which has been weakening again since early January.

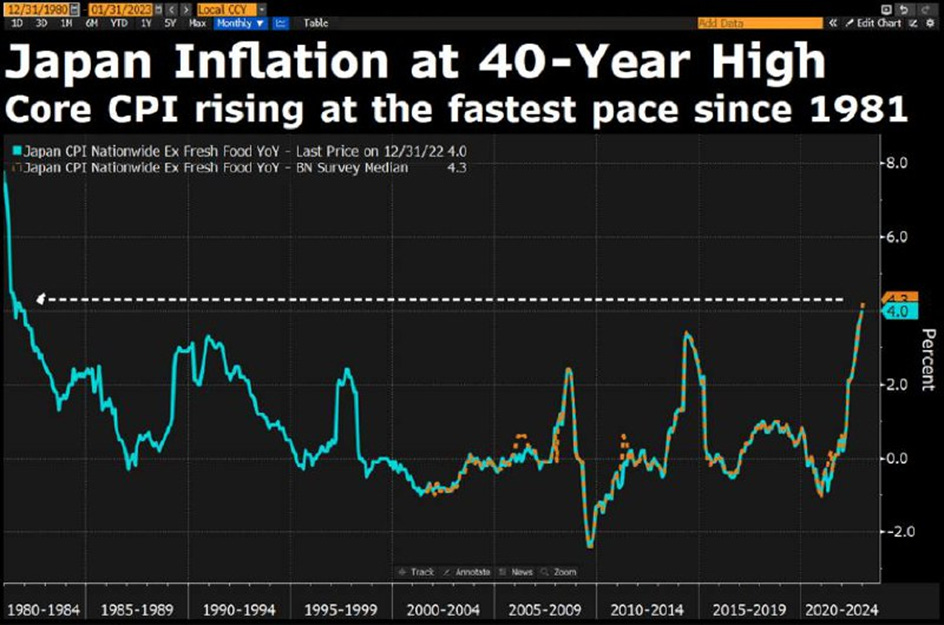

Given Japan inflation is already at 40 year high with core CPI rising at the fastest pace since 1981, we are wondering what the new Bank of Japan supremo Kazuo Ueda will do:

- Graph source Bloomberg

At the same time currency funds have been trimming their short yen shorts waiting probably to see what the new president of the Bank of Japan is planning to change with Japan’s monetary policy:

- Graph source Bloomberg

The Bank of Japan already owns 56% of the Japanese government bond market so we are indeed wondering like any good Cheshire cat what are they going to do next because Japan will boost its defense budget for 2023 to a record 6.8 trillion yen ($55bn), or a 26.3% increase, in the face of regional security concerns and threats posed by China and North Korea. The difference between Japan going from 1% of GDP to defense to 2% from amounts to spending on the order of $500 billion (in 2020 U.S. dollars). To fill this gap in the next five years, Japan would need to invest an additional 2 percent of GDP on top of planned increases just to offset one decade of underspending. How are they going to fund this increase could have serious implications for financial markets in general and Fixed Income / Credit markets in particular. A corporate tax hike would force companies to reconsider wage increases which would not be consistent with what is advocated by the Kishida administration. Most Japanese support apparently expanded defense spending but, remain reluctant to accept tax hikes. The easiest route would be of course to issue more bonds and this would obviously have an impact on the already bloated balance sheet of the Bank of Japan.

If the Bank of Japan allows Japanese yield to rise, Japanese investors would most likely repatriate their cash and liquidate their foreign holdings. Rapid population aging reduces saving rates and prompt the country to draw down on its net foreign assets. The implementation of NIRP by the Bank of Japan and Kuroda’s policies for 10 years induced more foreign bonds buying by the Japanese Government Pension Investment Fund (GPIF) as well as Mrs Watanabe (analogy for the retail investors) under Kuroda.

Back in March 2015 in our conversation "Information cascade", we stressed the importance of following what the Japanese investors were doing in terms of flows:

"Go with the flow:

One should closely watch Japan's GPIF (Government Pension Investment Fund) and its $1.26 trillion firepower. Key investor types such as insurance companies, pension funds and toshin companies have been significant net buyers of foreign assets." - source Macronomics, March 2015

If savings rates are falling and if inflation is accelerating in Japan as well what will the GPIF do in terms of “allocation” and what will Mrs Watanabe do through her Toshin funds? Japanese investors have been heavy buyers of US corporate bonds since 2012!

So, all in all, after many years of playing the “sorcerer’s apprentices”, the Fed, the ECB and the Bank of Japan are facing huge issues in exiting their ultra-loose monetary policies. One thing for sure, it will be painful.

“Only a few find the way, some don’t recognize it when they do – some… don’t ever want to.” – Cheshire Cat

You can join Macronomics on our Telegram Channel indicated in our Twitter profile as well you can join our Twitter feed. Going forward we will publish more frequently on our dedicated Substack page.

PERSONAL COMMENTS ON MACRO TRENDS, MACRO NEWS AND VIEWS. ALL RIGHTS RESERVED. DISCLAIMER: INFORMATION PROVIDED ON THIS BLOG DOES NOT CONSTITUTE A RECOMMENDATION OR ADVICE TO PURCHASE ANY INVESTMENT, PRODUCT OR SERVICE LISTED OR MENTIONED ON THIS BLOG. INFORMATION DISPLAYED ON THIS BLOG IS NOT INTENDED AS SPECIFIC INVESTMENT ADVICE AND SHOULD NOT BE RELIED ON FOR MAKING INVESTMENT DECISIONS.

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Martin - Vous ne cesserez jamais de me surprendre. The Cheshire Cat Effect aka a glitch in the Matrix, which causes counterfactual information to be transmitted, perceived and reacted to. There are no accidents or coincidences in life - everything is synchronicity and none of this is by happenstance.

Martin - Vous ne cesserez jamais de me surprendre. The Cheshire Cat Effect aka a glitch in the Matrix, which causes counterfactual information to be transmitted, perceived and reacted to. There are no accidents or coincidences in life - everything is synchronicity and none of this is by happenstance.