Reverse Polarity

“Hatred, anger, and violence can destroy us: the politics of polarization is dangerous.” - Rahul Gandhi

Looking at the gyrations in the US Treasury markets creating havoc in VaR calculations and therefore significant losses in Global Macro Hedge Fund on the back of renewed pressure on US regional banks in general and Credit Suisse in particular, with the Fed stepping in with other central banks, when it comes to selecting our title analogy, we decided to go for “Reverse polarity”. Reverse polarity is when the hot and neutral wires on a receptacle/outlet are wired “backwards.” In other words, the hot (black) wire is where the neutral wire should be, and the neutral (white) wire is where the hot wire should be. This results in a shock/electrocution hazard. As such, the Fed latest intervention, in similar fashion to “reverse polarity”, “Electronic equipment” or “banks” plugged in to an outlet/central bank with reversed polarity will still function, but that doesn't mean it will be safe.

In this conversation, we would like to discuss current banking woes in general and Contingent Capital Bonds (aka CoCos / AT1) being short gamma in particular.

· Banking woes à la Savings & Loan crisis in the US

While many financial pundits have been claiming and fearful about a return of the Great Financial Crisis à la 2008, we think that this comparison is not accurate relative to the current “inflationary” set up and hiking path of the US Fed. What is happening to the regional banks in some instances is similar to the savings and loan crisis of the 1980s and 1990s. As a reminder, starting in October 1979, the US Fed raised the discount rate that it charged its member banks from 9.5% to 12% in an effort to reduce inflation. At that time, S&Ls had issued long-term loans at fixed interest rates that were lower than the newly mandated interest rate at which they could borrow. When interest rates at which they could borrow increased, the S&Ls could not attract adequate capital from deposits and savings accounts of members for instance. Attempts to attract more deposits by offering higher interest rates led to liabilities that could not be covered by the lower interest rates at which they had loaned money. The end result was that about one third of S&Ls became “insolvent”. When the problem became apparent, after the Fed increased interest rates, some S&Ls took advantage of lax regulatory oversight to pursue highly speculative investment strategies:

“Financial historian Kenneth J. Robinson, in his explanation of the crisis published in 2000 by the Federal Deposit Insurance Corporation (FDIC), offers multiple reasons as to why the S&L crisis came to pass. He identifies rising monetary inflation beginning in the late 1960s and increasing through the 1970s, caused by the federal government's domestic spending programs implemented by President Lyndon B. Johnson's "Great Society" programs and the federal government's mounting military expenses for the Vietnam War that continued into the late 1970s. The Federal Reserve's efforts to reduce rampant inflation of the late 1970s and early 1980s by raising interest rates brought on a recession in the early 1980s and the beginning of the S&L crisis. The Federal Reserve's policies to increase the discount rate charged to other banks, compared to the long-term fixed rates of loans the S&Ls had already made, practically ensured that most S&Ls would become insolvent very quickly." – source Wikipedia

The rapidity of the hikes of the US Fed led indeed to an asset and liability mismatch for many weakened and yes, poorly regulated entities such as Silicon Valley Bank.

As such the recent turmoil in US Regional banks is similar to the Savings & Loans issues of the past in terms of assets and liabilities mismatch particularly in the light of their Commercial Real Estate exposure which increased in recent years:

- Graph source Macronomics – Refinitiv Eikon

In our previous conversation we pointed out that in the last 10 years US banks thanks to the different path of their respective central banks have led to a different outcome relative to Europe. In the United States the deleveraging was more rapid and quite significant:

- Graph source Macronomics – KOYFIN

As you already know our “stagflationary stance” in numerous musings of ours, clearly the ongoing situation for US Regional Banks is eerily reminiscent of the Savings & Loan crisis. We would therefore not be surprise to see more regional banks failures in the coming months based on this historical perspective. The US Fed is facing both inflationary and financial stability headwinds, but, in the respect of “inflationary” headwinds the ECB is in a much more difficult position as we have opined recently.

Of course, a cause for concern is the exposure of these regional banks to Commercial Real Estate (CRE). We already have seen some significant players in that space going for “strategic defaults”. Smaller banks hold about 70% of CRE loans (or commercial mortgage-backed securities). CRE appears increasingly vulnerable as a result with $1.5 trillion in commercial real estate debt maturing in the next three years. Banks are already tightening lending standards for CRE loans as per the most recent quarterly Fed Senior Loan Officer Opinion Survey (SLOOs):

- Graph source Federal Reserve Board and Wells Fargo Economics

This is of course leading up to significant “repricing” in the CMBS space. No wonder Blackstone’s Global Head of Private Wealth Solutions Joan Solator is sounding the alarm on traditional office space. Remember that failing Signature bank has significant exposure to commercial real estate. As such FDIC still needs to find a buyer for this core commercial real estate loan portfolio. Signature Bank’s partial takeover by a competitor is notable for what it doesn’t include: $11 billion of loans against a class of New York City apartments whose values have tumbled in recent years. New York Community Bank has effectively snubbed Signature’s bank CRE loans portfolio. This is significant given Signature Bank held a 12% share of the CRE lending market in the New-York metro area. Trepp Bank Navigator estimated that $25.5 billion of Signature Bank’s $35.2 billion CRE portfolio was made on properties in the New-York metro area.

As pointed out by Daniel McNamara on our twitter feed:

“This year will be critical because about $270 billion in commercial mortgages held by banks are set to expire, according to Trepp - the highest figure on record. Most of these loans are held by banks with less than $250 billion in assets. In a recent paper, a group of economists including Mr. Piskorski estimated that the value of loans and securities held by banks is around $2.2 trillion lower than the book value on their balance sheets.” – Daniel Mc Namara

No wonder CMBX 15 BBB- is plunging even more in this context:

- Graph source- ZeroHedge – Bloomberg

CMBX 10 to 16 have the largest concentration to office loans. The CMBX is an index that tracks the performance of a group of commercial mortgage-backed securities (CMBS), which are bonds backed by a pool of commercial mortgages. These indices are used by investors to gain exposure to the CMBS market and to “hedge” their risks:

- Graph source Bloomberg

In 2008 during the Great Financial Crisis, Big Short 1.0 was in RMBS and famous investor Michael Burry was made famous by buying CDS on RMBS. Big Short 2.0 was in March 2017 on Retail Commercial Centers via CMBX series 6 which was a very profitable trade for Carl Icahn. Big Short 3.0 was in spring 2020 shorting exposure on hotels via exposure to CMBX series 9. Now indeed it seems to us that Big Short 4.0 is indeed via exposure to CMBX 10 to 16 but we ramble again.

On a side note, looking at the events unfolding in our home country France with riots, strikes and more, we are more and more vindicated in by our “pre-revolutionary” mood. Inflation goes hand in hand with discontent as shown during the Arab Spring which was triggered by QE2 in March 2011 which was highlighted in a paper work by the Bank of Japan as a reminder.

· Being “short gamma”

First we have to confide that we always had a profound “aversion” for CoCo bonds (Contigent Capital Notes) for being in effect a “short gamma” position for an investor and also for its poor risk/reward "beta" proposal. Any decent trader will tell you that you never want to have a big negative gamma position.

We would like to remind ourselves again in the context of the Credit Suisse CoCo saga the wise words of Dr Jochen Felsenheimer we quoted in a previous conversation relating to banks, government and mis-pricing of risk:

"Banks employ too much debt, because they know that they will ultimately be bailed out. Governments do exactly the same thing. Particularly those in currency unions with explicit - or at least implicit guarantees. It is just such structures that let government increase their debt at the cost of the community. For example, in order to finance very moderate tax rates for their citizens so as to increase the chance of their own re-election (see Italy). Or to finance low rates of tax for companies and at the same time boost their domestic banking system (see Ireland). Or to raise social security benefits and support infrastructure projects which are intended to benefit the domestic economy (see Greece). Or to boost the property market (Spain and the USA). This results in some people postulating a direct relationship between failure of the market and failure of democracy." – Dr Jochen Felsenheimer

As long as governments agree to treat AT1s as debt rather than equity, interest payments out of pretax earnings make them cheaper to issue than stock for banks.

We discussed that very subject of equity buffers in our conversation "Dumb buffers" back in March 2013:

"The beauty for the issuer is that the CoCo automatically boosts its Core Tier 1 capital ratio in times of stress rather than being forced into a dilutive right issue during difficult market conditions. Owning a CoCo, according to a recent BNP Paribas note is very similar to selling a Down-and-In put option on the issuing bank’s shares with a knock-in barrier linked to a balance sheet capital ratio as opposed to stock price level.

The issuing bank is effectively buying skew and convexity (crash protection) from the investor, who is exposing himself to losses in stress scenarios.

It is not a free lunch although a coupon in the region of 7% to 8% is outright appealing in this low rate / low yield environment." - source Macronomics

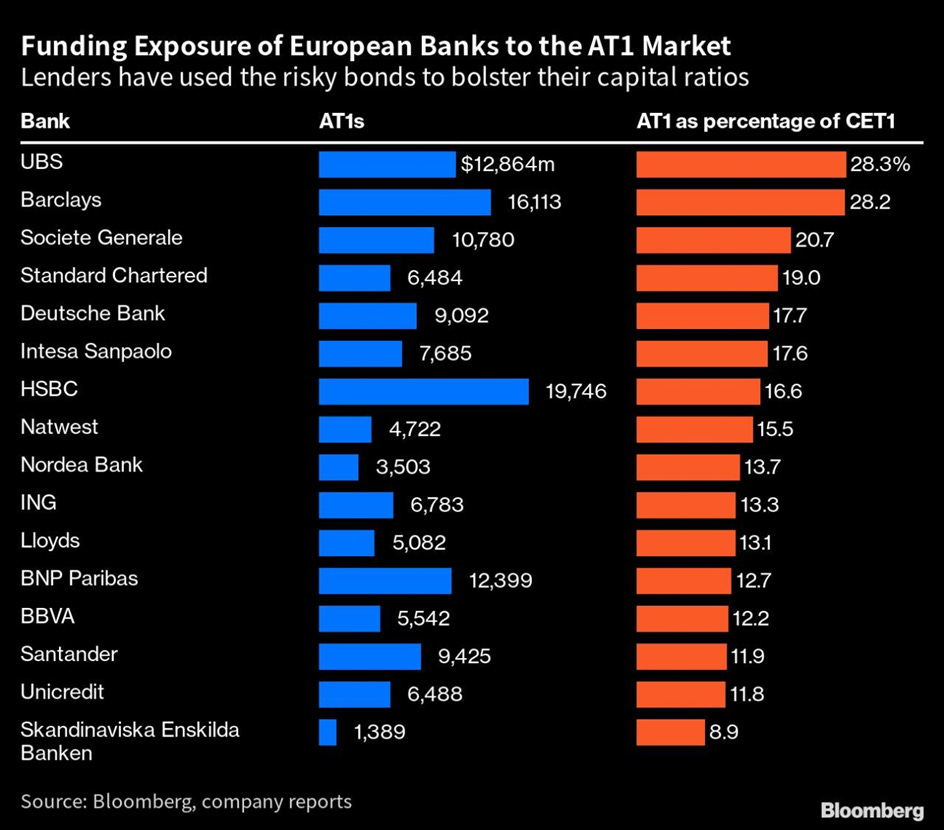

Given we like to give nicknames not only to central bankers but sometimes to some specific credit products, we indeed called these notes “Credit Molotov Cocktails”. By issuing CoCos with the complacency and support from regulators given that under European Union rules, banks can count additional Tier 1 debt equivalent to 1.5 percent of assets weighted by risk when calculating certain ratios, banks have been indeed issuing more "Molotov Cocktails" ($275 billion until the Credit Suisse write-off of $17.3 billion) rather than building true “equity buffers”:

- Graph source Bloomberg

This what we wrote in 2013 in our conversation “Dumb buffers” relating to CoCos:

“The fixation bankers have with equity buffers mean that they prefer issuing hybrids securities such as CoCos rather than equity in order to maintain their leverage and generate ROE. As indicated by Dr Jochen Felsenheimer, in case of trouble, the insurer is the taxpayer. CoCos are deemed to be "capital" and automatically improve the capital ratios, pleasing regulators in the process, and avoiding an automatic dilution of existing shareholders via capital increases through right issues. They are not equivalent to "equity", they are debt instruments, paying no doubt, a higher coupon, given the risk taken by the low subordination and risk of capital wipe-out faced by the bondholders.

As a reminder, under the draft Basel III plan in 2010, banks would have to hold so-called Tier 1 capital equivalent to 3 percent of their assets, so capping a lender’s debt at no more than 33 times those reserves, which, we think is way too low.” – Macronomics, 2013

Returning to the “velocity” of the demise of Swiss banking giant Credit Suisse it can be very simply explained by the negative gamma nature of the Credit Molotov Cocktail aka CoCos. We saw the same pattern with the demise of Banco Popular as pointed out by Risk Concile paper from the 16th of June 2017:

“When a CoCo bond drifts into a lower price range, this may stimulate professional investors to hedge their holdings through a short position in the underlying equity of the bank. This hedging activity may push the share price lower. As a consequence, this could have a negative impact on the bank's CoCo which in turn drives the hedgers to sell even more shares. This sets of a wave of uncontrolled selling, a death spiral is born.” – Risk Concile

In effect, the bigger the pressure on the CoCo bond, the bigger the selling pressure on the stock. What happened to Credit Suisse is similar to the demise of Banco Popular. Both AT1 and tier-2 investors lost everything when Banco Santander rescued Banco Popular, while senior bondholders were untouched. The rescue has shown that when banks in Europe get into trouble it is “liquidity”, not “capital”, that matters and that the fate of subordinated bondholders is anything but predictable! Banco Popular's situation showed us before that the fate of subordinated bondholders actually has very little to do with the precise structure of the instruments that they are holding:

- Graph source Bloomberg

Neither of Banco Popular’s Tier-1 notes had breached their triggers before the SRB decided that the bank had become non-viable. At the time European Central Bank (ECB) vice-president Vitor Constâncio clearly stated that the bank’s solvency was not the issue:

“There was a bank run. It was not a matter of assessing the developments of solvency as such, but the liquidity issue.”

Depositor withdrawals caused the SRB to deem the bank to be failing or likely to fail under Article 18 of the Single Resolution Mechanism Regulation. This meant that it had hit the point of non-viability (PONV).

Investors in AT1 instruments should, therefore, be paying much closer attention to the PONV language in their documentation than to “trigger language”. In general, about the treatment of shareholders relative to the CoCo bond holders in the Credit Suisse resolution, we believe that it is the job of the investors to read the “fine print” of the bond offering prospectus. It is the fiduciary duty of the investor/asset manager. For example, the perception of the credit worthiness on Dubai World before the restructuring was all about implicit guarantees from the Dubai Government which was never “explicit” in the offering memorandum. Investors invested believing in “implicit” support. Probably the same investors who believed in the sacro-saint AAA rating issued on dodgy CDOs and CLOs as a gauge of credit quality of the underlying pool of assets in the structure. Probably the same investors who believed that a callable LT2 bond will be called on the call date by the issuer, because it has been market practice. How surprised were bond investors when Deutsche Bank, in December 2008, decided not to redeem some sub debt on the date of the call!

When a takeover deal that blows through the latter is hammered out overnight there is not a lot that you can do as what happened again with Credit Suisse:

- Graph source Bloomberg

The market has long discussed about the death spiral effects in the CoCo market – whereby debt investors which are converted into equity on breach of a trigger are forced to immediately sell that equity and accelerate the demise of the institution. In Banco Popular case, and yes, we have a good memory, bondholders did not have time to be converted into anything that could be “sold”. Both Banco Popular’s AT1s and tier 2s were converted into shares that were immediately written down to zero. As a reminder the Dutch bank SNS resolution in 2013 meant that Tier 1 bonds and LT2 losses also equated to 100%.

Both in Banco Popular's case and in Credit Suisse case the short end of the CDS curve was already inverted before the takeover:

- Graph source Bloomberg

In a 2017 conversation entiled “Circus Maximus” we wrote the following:

“If indeed AT1 are known unknowns, and are American options like short gamma trades, who really cares about the capital threshold trigger aka the strike price seriously? We don't and continue to dislike these bonds but hey, some might enjoy nonlinearity, we are not big fans.” – Macronomics, June 2017

You probably understand therefore our “dislike” for these “Credit Molotov Cocktails” because in effect, the position of the investor in a CoCo bond is that he is the one selling the insurance to the bank which as BNP pointed out is buying skew and convexity (crash protection).

“In every society, manufacturing builds the lower middle class. If you give up manufacturing, you end up with haves and have-nots, and you get social polarization. The whole lower middle class sinks.” - Vaclav Smil

You can join Macronomics on our Telegram Channel indicated in our Twitter profile as well you can join our Twitter feed. Going forward we will publish more frequently on our dedicated Substack page.

PERSONAL COMMENTS ON MACRO TRENDS, MACRO NEWS AND VIEWS. ALL RIGHTS RESERVED. DISCLAIMER: INFORMATION PROVIDED ON THIS BLOG DOES NOT CONSTITUTE A RECOMMENDATION OR ADVICE TO PURCHASE ANY INVESTMENT, PRODUCT OR SERVICE LISTED OR MENTIONED ON THIS BLOG. INFORMATION DISPLAYED ON THIS BLOG IS NOT INTENDED AS SPECIFIC INVESTMENT ADVICE AND SHOULD NOT BE RELIED ON FOR MAKING INVESTMENT DECISIONS.

Martin - as always tres magnifique!