Looking at what the wise bankers of the BIS are saying relating to valuations of Tech stocks may be reaching “extreme height again” when it came to selecting our title analogy we decided to go for a reference to Irving Fisher 1929 jubilant quote. On the 3rd of September 1929, the Dow Jones Industrial Average swelled to a record high of 381.17, reaching the end of an eight-year growth period during which its value ballooned by a factor of six. “Stock prices have reached what looks like a permanently high plateau,” Irving Fisher rejoiced in the pages of the New York Times.

In the 2007 classic book “100 minds that made the market”, Ken Fisher, unrelated to Irving Fisher said the following:

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

“Economist Irving Fisher left an abundant amount of work in mathematical economics, the theory of value and prices, capital and monetary theories, and statistics. Indeed, it seems almost as if he were touted as one of the great economists simply because he had a lot to say. He wrote at least 10 major books and taught at Yale for over 35 years. But credentials don’t always mean you’re right. In fact, in Fisher’s case, credentials allowed him to be wrong in a number of his major hypotheses like the 1929 Crash-and then spring back with revised jargon after the fact. Clearly, Fisher’s greatest contribution to Wall Street was his own negative example which should stand as a permanent warning to all concerned with financial markets and economics to steer clear of what economists have to say. Since Fisher’s day all kinds of studies have demonstrated that economists are wrong more often than right.” – Ken Fisher

Irving Fisher’s biggest blunder, beyond any doubt, came with his infamous 1929 call one week before the Crash and ensuing Depression.

In this conversation we would like to look at price action in BitCoin gold and various asset classes given the continuation of the “risk-on” environment.

Our long monthly musings are now for paid subscribers only and a new one will be published soon.

This shorter than usual article is free, so don’t hesitate to share it and if you like our work don’t hesitate to subscribe.

Don’t hesitate to reach out if you have any questions or suggestions.

· Everything glitters including gold

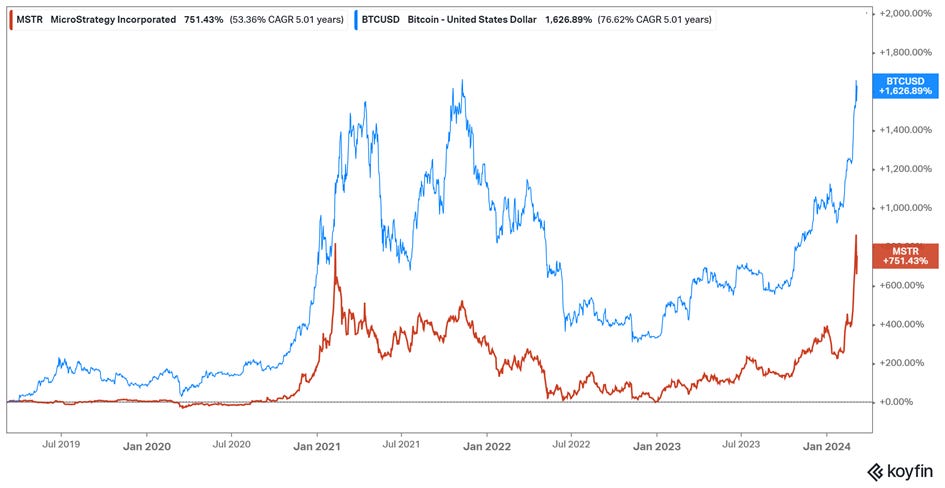

As we pointed out in our conversation “The Year of the Dragon”, we have followed MictroStrategy (MSTR) as being a “derivative” of BitCoin and being somewhat more volatile yet underperforming BitCoin over the last 5 years:

- Graph source Macronomics – KOYFIN

Yet the 3 years picture clearly displays a different picture “performance” wise:

- Graph source Macronomics – KOYFIN

And, year to date (YTD), in effect, MSTR is outperforming significantly BitCoin by a significant margin and even more on a one month basis (+137% for MSTR vs +56.5% for BTC):

- Graph source Macronomics – KOYFIN

We indicated in our January conversation that the CEO of MSTR had started cashing in on his holdings, the first time in nearly 12 years. We also discussed rising “insider selling” in our previous conversation with Jamie Dimon from JP Morgan selling for the first time since 2005 and the reason probably behind it (Fiscal Dominance and bond stuffing):

- Graph source Bloomberg – X/Twitter

MSTR raised $700m at 0.625% per annum due in 2030, with a convertible boasting a strike price 40% higher than where the stock closed yesterday. All the proceeds going towards buying more $BTC. In January we were wondering given the introduction of ETFs on BitCoin if MSTR would stop becoming a “proxy” short or “long”. On the contrary, the latest convertible bond issue is going to make it even more “beta” sensitive to BitCoin.

In our last musing we touched on the subject of “Market concentration”:

- Graph source: Jeffrey Kleintop - Financial Times – X/Twitter

Concentration risk per se is not how much of an index that the top ten stocks account for since some markets have fewer stocks. Unlike the 500 stocks in the S&P 500, the MSCI Germany index only has 53 stocks as pointed out by Jeffrey Kleintop, CIO of Charles Schwab on our X/Twitter feed. Therefore it is not surprising to see more of the index market cap in the top 10 stocks for Germany but, as we stated in our last conversation, performance wise, Developed Markets (DM) such as the S&P500 display high level of “concentration” in the TECH space, the concentration we can see in indices such as in Emerging Markets (EM) such as the IBOV index. This is why we are saying DM is the new EM.

Jeffrey Kleintop also made this very important points:

“The real concentration risk is how much of the performance of an index is coming from just a handful of stocks.

We can see from the capitalization and equal-weighted indexes that Europe's stock markets, while much more concentrated in the top stocks, isn't concentrating its performance in the top stocks (the cap and equal weight indexes are performing similarly). But the US is and that is creating a vulnerable gap between the performance of a handful of the largest stocks and all the others.” – Graph source Charles Schwab – Jeffrey Kleintop – X/Twitter

In a side note of our last conversation we pointed out that both AI and BitCoin depended on silver for hardware. Looking at the below 5 years chart, we are getting kind of bullish as well on Palladium (in red):

- Graph source Macronomics - KOYFIN

As you know Palladium’s key commercial use is as a critical component in catalytic converters - a part of a car's exhaust system that controls emissions - found mainly in petrol and hybrid vehicles. What we find of interest is that second hand EV price’s represent massive depreciation. A discounted EV is same price as its discounted Petrol equivalent these days. This has a very negative impact on new EV car sales and makes finance deals expensive (yes, interest rates matter in the space as well). This leads to heavy discounts on new car sales cutting profit margins and at the game of “cutting prices”, it is a game China is currently winning (BYD vs TESLA).

“The oil price cap or EU ban on sale of new petrol and diesel cars from 2035 do not seem to take into account “dynamic supply” (An EV requires 2.5 times as much copper as an internal combustion engine vehicle). On average, an EV needs between 6kg and 12kg of cobalt, which translates to about 120,000 tonnes a year. More than 70% of the world's cobalt is produced in the Democratic Republic of Congo, and any nation that produces electronics wants in on that source. But, based on operational mines and projected demand, forecasters predict that supply won't be able to keep up with demand by 2030, or even as early as 2025. For electric cars (EV) you need to source commodities in “size” and we are not even discussing the urgent need for new nuclear plants. Unfortunately for us, our current batch of leaders live in a “different reality” and do not seem to grasp basic economic theory when it comes to commodities supply and inventories, end of our rant.“ – Macronomics – November 2022

A combustion engine car for the time being continue to have more “residual value” as scrap metal. EV batteries are still very expensive to replace and to recycle. Add to this that is almost impossible to detect battery damage after even a minor accident. Remember that Hertz took the decision to drastically cut its EV exposure thanks to its epic depreciation problem which caused a loss for the company last quarter. Hertz followed up by halting plans to buy 65,000 electric cars amid EV slump. Morgan Stanley in a recent note indicated the following (H/T Carl Quintanilla):

“.. EV demand continues to decelerate despite continued price cuts. Fleets are dumping EVs and strong hybrid momentum is competing for the marginal EV buyer. Could $TSLA lose money (sometime) this year?” [Jonas] – Morgan Stanley

Aston Martin also admitted that drivers don’t want “electric cars”. Yet another carmaker delaying EVs and shifting to Hybrid/Plug-in Hybrid vehicles.

So, you probably understand why we are contrarian “bullish” on Palladium, to play the “Hybrid” game. Stock wise, if you want to play it, Toyota seems to us that it has been the right place to be as per the one year chart below (Toyota vs TESLA):

- Graph source Macronomics – KOYFIN

Short TESLA / Long Toyota and Palladium? We wonder…

When it comes to “glittering”, gold is finally breaking out as per the below chart from Sagar Singh Setia on our Linkedin feed:

“This Is Unprecedented! Gold has broken a two-decadal-old correlation with the real yields in the last two years.

Despite higher real yields, Gold prices have been stable at around $2000.

However, as we get near to cuts by the Fed and real yields move down again, the rise in the shiny yellow metal can surprise everyone.”

One of the best diversification bets! Isn’t it?”- Graph source Sagar Singh Setia

Everything glitters, S&P500, Dax, CAC40, credit, BitCoin and gold included. Permanent high plateau?

With Geoffrey’s help, we endeavor to touch more on various subjects through GRAPHFINANCIALS. Should you have any question, don’t hesitate to reach out to us.

The future is inherently full of discontinuities, and lessons of the past must be applied with enormous caution. Zbigniew Brzezinski

You can join Macronomics on our Telegram Channel indicated in our Twitter profile as well you can join our Twitter feed. Going forward we will publish more frequently on our dedicated Substack page.

PERSONAL COMMENTS ON MACRO TRENDS, MACRO NEWS AND VIEWS. ALL RIGHTS RESERVED. DISCLAIMER: INFORMATION PROVIDED ON THIS BLOG DOES NOT CONSTITUTE A RECOMMENDATION OR ADVICE TO PURCHASE ANY INVESTMENT, PRODUCT OR SERVICE LISTED OR MENTIONED ON THIS BLOG. INFORMATION DISPLAYED ON THIS BLOG IS NOT INTENDED AS SPECIFIC INVESTMENT ADVICE AND SHOULD NOT BE RELIED ON FOR MAKING INVESTMENT DECISIONS.

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Martin - another capolavoro.