“I have often said that just as the French revolution, for instance, understood itself through antiquity, I think our time can be understood through the French revolution. It is quite a natural process to use other times to understand your own time.” - Ian Hamilton Finlay

Watching with interest the renewed unrest in my home country France, following the much rejected pension reform in conjunction with gold prices getting near a monthly $2000 close, on top of Bank of England chief economist Huw Pill saying that Britons “need to accept” they are poorer, when it came to selecting our title analogy we obviously had to go for a French revolutionary one, namely “Let them eat cake”. "Let them eat cake" is the traditional translation of the French phrase "Qu'ils mangent de la brioche", said to have been spoken in the 18th century by "a great princess" upon being told that the peasants had no bread. The French phrase mentions brioche, a bread enriched with butter and eggs, considered a luxury food. The quote is taken to reflect either the princess's frivolous disregard for the starving peasants or her poor understanding of their plight. While the phrase is commonly attributed to Marie Antoinette, it was coined by 1765, when she was 9 years old and had never been to France, and it was only attributed to her decades after her death. It is unlikely that she ever said it but was mentioned in the book Confessions of French philosopher Jean-Jacques Rousseau. As one biographer of Queen Marie Antoinette notes, it was a particularly powerful phrase because "the staple food of the French peasantry and the working class was bread, absorbing 50 percent of their income, as opposed to 5 percent on fuel; the whole topic of bread was therefore the result of obsessional national interest”. There were two serious bread shortages in France prior to the French Revolution, the first in April–May 1775, a few weeks before the king's coronation on 11 June 1775, and the second in 1788, the year before the French Revolution.

For those who have been faithful readers of our musings, you know our “pre-revolutionary mindset” when it comes to our views of current circumstances. In various musings of ours we have made many references to the similarities of the current stagflationary plights and inflationary risks on social stability such as in our August 2022 conversation “General Maximum” or in our 2016 conversation entitled “Thermidor”. Given the quote is taken to reflect either the princess's frivolous disregard for the starving peasants or her poor understanding of their plight, when we read Huw Pill’s comment on the poor Britons plight, we are wondering if indeed the chief economists or some central bankers could face a similar fate of the French royal family during the French Revolution, but we ramble again.

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

In this conversation, we would like to discuss the subject of “dedollarization” and the link to commodities, SVB and Bank of Amsterdam as well as the stagflationary environment in the light of the most recent US GDP print of the 1st quarter at 1.1%.

· Dedollarization, SVB and Bank of Amsterdam

Before delving into the nitty gritty of “dedollarization”, we would like to point out to historical similarities of the current context with the French Revolution as pointed out by the quote we have used above. In our previous musing entitled “Thermidor”, we indicated the work of French economist Florin Aftalion and what characterized the proper French revolutionary period (1789-1794) wich was poor harvests and very similar meteorological factors witnessed in 1788 and 1789, namely very hot spring-summer periods with very bad weather followed by very cold winters (-21 degrees Celsius in Paris during the winter of 1788). On a side note Florin Aftalion is the author of “The French Revolution - An Economic Interpretation", a must read in our opinion. As such and in continuation to our historical reference of the current period of “droughts” and global warming events leading to social unrests, we read with interest Maria Waldinger July 19 2021 paper entitled “Let them Eat Cake – Drought in 1788 and political outcomes in the French Revolution”. Her paper studies whether a drought in 1788 affected the outbreak of peasant and the results of course provides similar evidence than Florin Aftalion’s work (which Maria Weldinger seems unaware of) in the sense that indeed the weather pattern at the time had an impact on triggering the French Revolution:

“In the 1780s, France was in deep economic and political crisis for a number of long and medium-term reasons. After years of warfare and an exuberant lifestyle at the French court, France's Financial resources were exhausted. The highly inefficient tax system exempted the rich and overburdened the poor. It was firmly in the hands of the nobility and did not generate sufficient income for the state. When the French king sought to reform the rigid and inequitable tax system, which would have reduced the nobility's income from taxation, a lengthy dispute between the king and the French nobility ensued. The members of French nobility were not willing to agree to reform unless the king considerably increased their political power (Hoffman and Rosenthal, 2000). In 1788, a drought hit France and caused severe crop failure. Grain prices soared. A growing part of the population went hungry. As France was already in deep economic and political crisis, the French king Louis XVI had limited means to import grain from aboard or to quell public discontent using military means. While grain prices continued to rise public discontent grew. By summer 1789, open revolt against the feudal ancien régime had broken out. Several historians have hypothesized that the drought of 1788 and ensuing harvest failure affected the course of the French Revolution (Le Roy Ladurie, 1971; Lefebvre and White, 1973; Neumann, 1977; Neumann and Dettwiller, 1990). ” – Maria Weldinger

On a side note, in our last musing we pointed out that inflation was going hand in hand with discontent as shown during the Arab Spring triggered by QE2 in March 2011 which was highlighted by the Bank of Japan.

You might already be wondering where we are getting with our historical references, SVB and the Bank of Amsterdam, the French Revolution and “dedollarization”.

As per our good friend Geoffrey Fouvry rightly asked on his twitter feed (@GraphFinancials), can we compare the failure of SVB to the failure of the Bank of Amsterdam during the Napoleonic wars?

“The resilience of the Bank of Amsterdam and its success over many decades came under pressure in the late 1770s. Under the economic stresses generated by war with the English, the Bank departed more seriously from sound practice by lending on a more substantial scale to the VOC, in a sustained and non-transparent way. Crucially, unlike a modern central bank that has the fiscal backing of the sovereign, the Bank of Amsterdam lacked fiscal backing. While the Bank’s public sector ownership by the city of Amsterdam gave it some degree of fiscal support from the city tax authorities (and also the ability to mutualise losses across segments of Amsterdam society), this was not sufficient for the large scale of activities of the Bank given the large volume of international trade through Amsterdam. The Bank operated with slightly negative equity for most of its existence, but did not have safeguards for when equity turned more deeply negative. In particular, the actions of municipal authorities to receive profit distributions of the Bank without a symmetric recapitalisation flow in times of losses cast doubt on the value of the municipal backing for the sustainability of the Bank’s solvency.

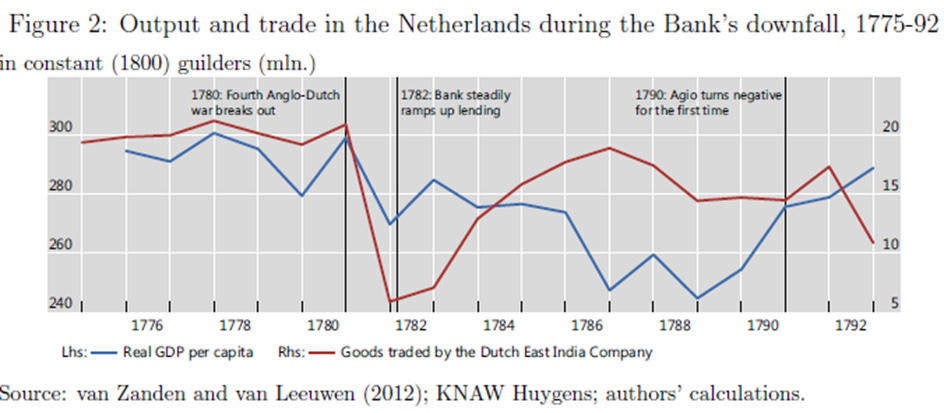

The pivotal event was the shock of the Fourth Anglo-Dutch war (1780-84) which led to extensive naval confrontations between the Dutch Republic and England in several theatres of conflict - in European, West Indian and Asian waters. This conflict was an economic shock that strained the VOC, which had become the main borrower of the Bank of Amsterdam. Shipping volumes by the VOC fell dramatically; sales of trade goods in the Netherlands dropped from 20.9 million guilders in 1780 to only 5.9 million in 1781.

Amid dire and deteriorating economic conditions, the Bank commissioners made the fateful decision to start granting even larger overdrafts to the VOC. As a result, the credit exposure of the Bank rose from 0 in June 1779 to 4.8 million guilders in 1781. The Bank then temporarily stopped new lending, but the stock of loans to the VOC remained high. The slump in the VOC trade continued (Jonker and Sluyterman (2000)). High losses of ships meant that loans that were already extended could no longer be repaid.

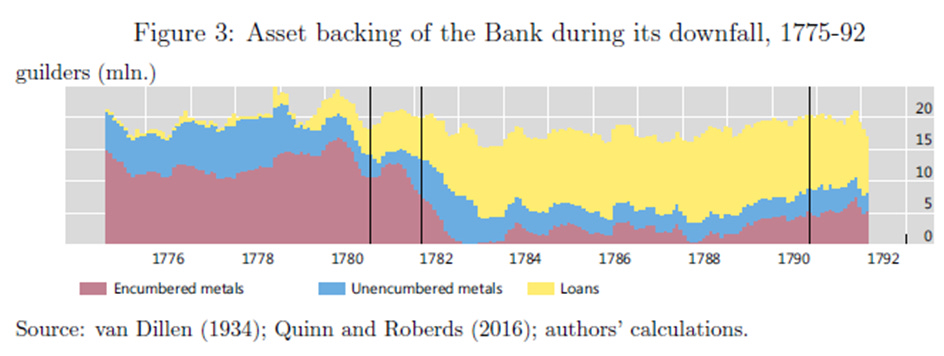

In May 1782, the commissioners decided to swap the suspended loans to the VOC into longer-term bonds (van Dillen (1934)). Throughout 1782, the Bank steadily ramped up its lending to the VOC; outstanding loans rose to a peak of 7.8 million guilders in February 1783. As loans increased (to a full 71% of the Bank’s assets), the metal stock fell, from 17.6 million guilders in 1776 to 7.8 million in 1783 (Figure 3).

This was because account holders with receipts redeemed coins by allowing their receipts to expire.

During the first half of 1783, the Bank responded to downward pressure on the agio by selling 3.5 million worth of guilder coins into the market (Quinn and Roberds, 2016).

By the summer of 1783, guilders were now only backed by metal coins for 28% of their value, from 97% just four years earlier. With the conclusion of the war in May 1784, the Bank had accumulated a large credit exposure which soon become non-performing.

The Bank’s insolvency - and the inability of the city authorities to recapitalise it - are important elements in its downfall. The Bank’s income sources comprised mainly fees from the receipt system and interest margins on loans. However, while the loans to the VOC became non-performing, the bank had not been rebuilding capital to cover these losses, as profits were regularly distributed to the city. Moreover, it had neither the seigniorage income of modern central banks, nor an adequate fiscal backstop. The city of Amsterdam did make limited attempts to recapitalise the Bank, but the funds were quickly diverted back to city coffers (Quinn and Roberds (2016)). From the perspective of modern central banking theory, the City of Amsterdam’s fiscal capacity was insufficient to provide the sovereign backing of an institution that had become a proto-central bank.

The extent of lending exposures remained opaque for a further decade, but market developments as indicated by the agio suggest that market participants were skeptical about the solvency of the Bank of Amsterdam. In July 1789, as the Bastille was stormed in Paris and uncertainty spread across Europe, the agio on the Bank guilder dropped to 2%, and eventually turned negative in October 1790–February 1791. It recovered briefly following a bond issue by the City of 6 million guilders for recapitalisation (van Dillen (1964)). Yet this recapitalisation was unsuccessful, in part because the city authorities - lacking adequate tax resources - soon diverted these resources to other uses (Quinn and Roberds (2015)).

The final chapter came in 1795, after the invasion of the Netherlands by French revolutionary armies. It was then that the true extent of the Bank’s insolvency came to light.” – source BIS

The Bank of Amsterdam persisted for two centuries and was widely used not only in the Netherlands but for trade across Europe and around the world. It was seen by many as the first global currency.

Second, as pointed out by our friend, SVB was not issuing deposits versus traditional banking products (since many startups would not qualify) but a mere bank for deposits. The bank had losses because of its holdings of government securities and went bankrupt after a deposit run. Here is what Henry Thornton considered as the father of central banking wrote on the Bank of Amsterdam in his book “An Enquiry into the Nature and Effects of the Paper Credit of Great Britain“:

“The bank of Amsterdam did not issue circulating notes, but was a mere bank for deposits, the whole of which it was supposed by some to keep always in specie. It was discovered, however, when the French possessed themselves of Holland, that it had been used privately to lend to a certain part of them to the city of Amsterdam, and a part to the old Dutch government. These loans ought certainly rather to have been furnished in that open manner in which those of our bank are made. Neither of the two debts, as I understand, have yet been discharged. The bank of Amsterdam had no capital of its own” – Henry Thornton

If you are connecting the dots, inflation was already on the rise following the fiscal largess distributed by the US government in the United States following the COVID crisis leading to a big surge in M2. The war in Ukraine added inflationary pressure on top and the Fed had to increase its hiking pace leading to the demise of SVB, in similar fashion that the Napoleonic wars following the French revolution led to the demise of the Bank of Amsterdam.

But why does all of this lead us to the theme of “dedollarization”?

In some instances and as pointed out by the paper from the BIS, Central Banks can operate with “negative equity” and many have done so in history without undermining trust in “fiat money”. But, as pointed out by the wise wizards of the BIS, there are limits, which it seems some sorcerer’s apprentices are oblivious to.

We agree with our friend Geoffrey Fouvry that the reason non G7 Central Banks have been holding so far US Treasuries is that it was superior paper to their own government debt. But the past plagues of some Emerging Markets have disappeared. For instances if we take Malaysia, there is neither a huge budget deficit nor a quasi fiscal deficit and most of its business is done in Asia and it has access to ample Yuan Swap lines. So why holding US Treasuries and not gold instead and their own government debt? Without US Treasuries, there is indeed less “imported inflation”.

Right now the US Fed is paying interest on parked reserves and is in “negative equity”. Quasi fiscal deficit of a central bank is what can lead to “hyperinflation” (Argentina), that is paying more interests on reserves than what you get from your assets.

As Rodriguez wrote at the World Bank:

“Paying interest on the monetary base or making Central Bank debt accessible to commercial banks may seem to be a good idea to increase the absorption of liquidity in the short run. The short run impact of printing money can be sterilized by imposing a higher remunerated reserve requirement or inducing banks to acquire other types of Central bank debt. However as this operation is repeated, the base for the inflation tax is eroded “ [because the inflation tax is returned in the form of interests and the Gov incurs a loss on its account at the Fed/ ] “and any additional deficit financing requires ever increasing rates of sterilization.”

The QFD (Quasi Fiscal Deficit) disease is traditionally at EM central banks, so it reinforces the point that if those central banks don't have this disease, why hold the Debt of a foreign central that has it?

As such the Fed is trapped given its negative equity position, it will need to restart QE unless the US Government takes drastic corrective action on its deficits. US Economic indicators are continuing to point to an ongoing weakening of the US economy, the fiscal position would be expected to deteriorate further as growth weakens and unemployment rises. We therefore understand Stanley Druckenmiller short USD position due to “unsustainable spending”.

As well, the debt ceiling debate is creating an arbitrage in the short end of the US yield curve, which steepens it, perversely helping banks to further pump leverage into the system!

For more on QFD we strongly recommend watching Geoffrey Fouvry’s take on GraphFinancials, a new venture in which we are participating as well.

Given the Chinese Yuan has overtaken the US dollar as most-used currency in China's cross-border transactions for the first time in history there are increasing talks about “dedollarization”. Yuan-share rose to a record high of 48%, up from nearly zero in 2010. U.S-share declined to 47%, down from 83% over the same period:

- Graph source Bloomberg

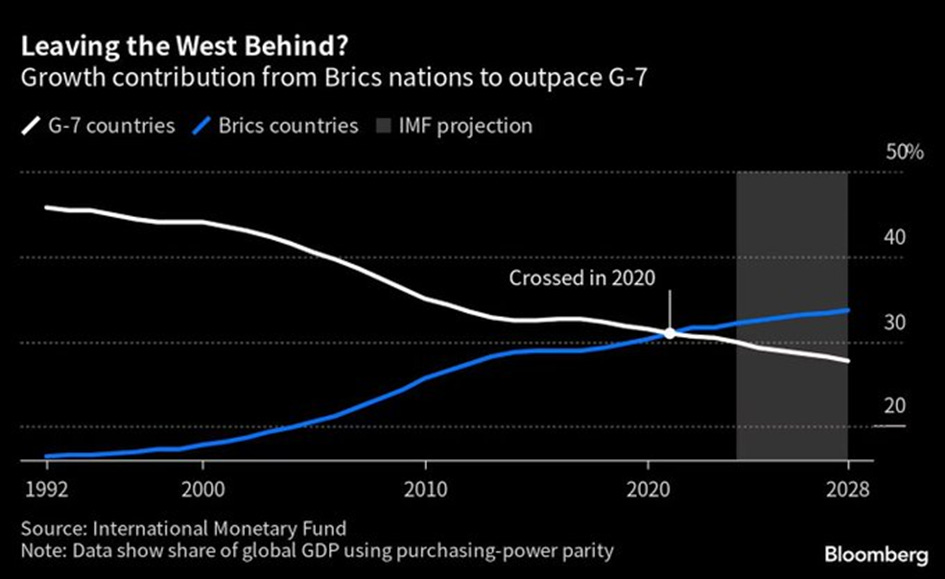

Growth of the BRICS is now as well outpacing the G7. BRICS will account for 32.1% of global growth this year, compared to the G7's 29.9%- as per IMF:

- Graph source Bloomberg

The weaponizing of the US dollar with as well the seizure of foreign reserves in conjunction with a significant rise in the US debt and out of control spending are of course leading to diversification of central banks reserves and no wonder many of them have been adding gold reserves in recent months.

When it comes to the subject of the “dedollarization” and commodities, the US Fed was successful in triggering commodities “repression” by maintaining very low interest rates, therefore enabling a cheap cost of financing for the shale players and their recovery following the oil price collapse in 2014-2015:

- Graph source Bloomberg

The issue of course is that out of the five major US shale basins, two are already past their prime, meaning that the “shale revolution effects” seems to be fading. As such, there is indeed potential for higher oil prices going forward, regardless of the “fossil fuel transition” narrative given the surge in demand from Emerging Markets, and this of course represent further inflation headache for central banks and it also means more entrenched inflationary pressure hence our “stagflationary” stance.

· Stagflation plays

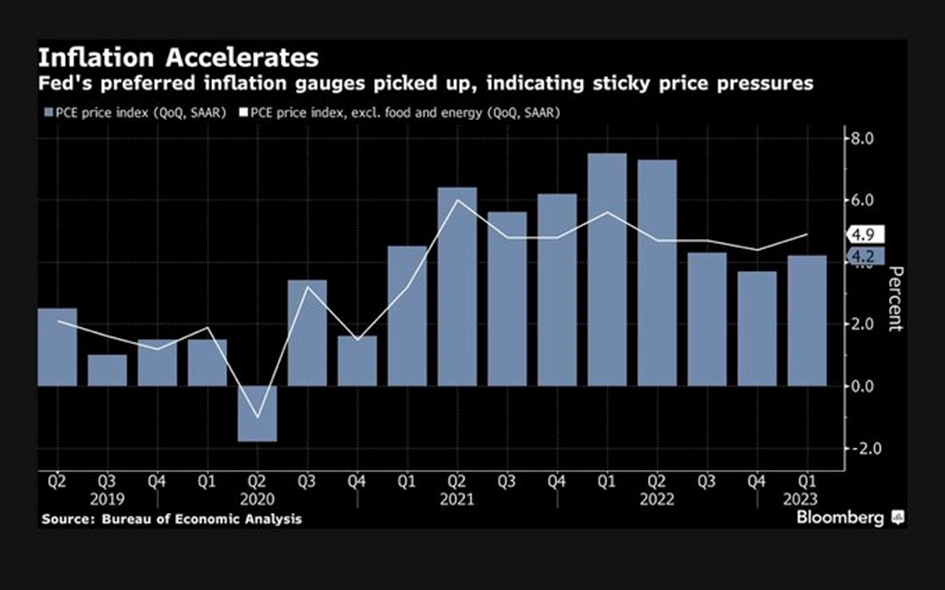

The US Q1 GDP miss at 1.1% came as well with a rise in the Fed’s preferred measure of inflation with Core PCE coming at 4.9%. This is of course giving more ammunition to our stagflationary talk:

- Graph source Bloomberg

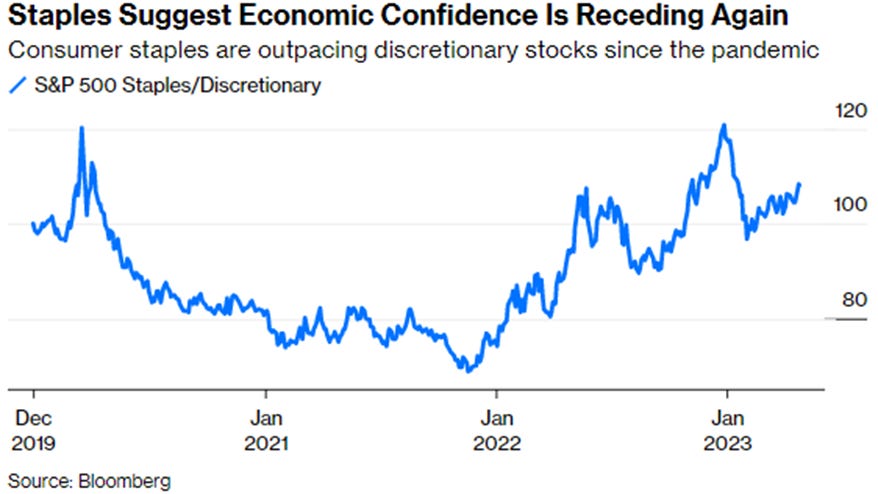

As well the relative performance of staples and consumer discretionary companies has traditionally been considered as a recession indicator:

- Graph source Bloomberg

In a stagflationary environment, you want to have Inflation-Linked Bonds such as US TIPS which also benefit from a deflation floor as well as exposure to gold and broad commodities. S&P 500 returns are dominated by the new economy: tech, platform companies, business services etc. The S&P is a bet on innovation, deflation and creative destruction. EMs vs. S&P is not a merely a bet on global growth but put it simply a sectorial bet: MSCI EMs returns are dominated by old economy industries, commodity- and more generally stuff-producing companies. EM equities are a bet on scarcity and inflation. As such, trade accordingly.

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.” - Henry Ford

You can join Macronomics on our Telegram Channel indicated in our Twitter profile as well you can join our Twitter feed. Going forward we will publish more frequently on our dedicated Substack page.

PERSONAL COMMENTS ON MACRO TRENDS, MACRO NEWS AND VIEWS. ALL RIGHTS RESERVED. DISCLAIMER: INFORMATION PROVIDED ON THIS BLOG DOES NOT CONSTITUTE A RECOMMENDATION OR ADVICE TO PURCHASE ANY INVESTMENT, PRODUCT OR SERVICE LISTED OR MENTIONED ON THIS BLOG. INFORMATION DISPLAYED ON THIS BLOG IS NOT INTENDED AS SPECIFIC INVESTMENT ADVICE AND SHOULD NOT BE RELIED ON FOR MAKING INVESTMENT DECISIONS.

Macronomics Newsletter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

N-gDp still above target. But there are some ominous signs. What derails economic expansion is a shifting of demand deposits to gated deposits.

Contrary to the myopic banker, from the standpoint of the system, banks create deposits, they do not lend them. This shifting destroys the velocity of circulation (because all bank-held savings originate within the system). I.e., the banks pay for the deposits that they collectively already own. This results in a consolidation of the banks.

Can you hear the sucking sound?

Small-Denomination Time Deposits: Total (WSMTMNS) | FRED | St. Louis Fed (stlouisfed.org)

Large Time Deposits, All Commercial Banks (LTDACBM027NBOG) | FRED | St. Louis Fed (stlouisfed.org)

Call it the paradox of thrift or precautionary savings. But from an accounting perspective, or flow, bank-held savings, stock, are frozen.

See: “Should Commercial banks accept savings deposits?” Conference on Savings and Residential Financing 1961 Proceedings, United States Savings and loan league, Chicago, 1961, 42, 43. By Dr. Leland James Pritchard, Ph.D., Economics, Chicago 1933, M.S. Statistics, Syracuse.

See: “Profit or Loss from Time Deposit Banking”, Banking and Monetary Studies, Comptroller of the Currency, United States Treasury Department, Irwin, 1963, pp. 369-386

re: "Paying interest on the monetary base" Remunerating interbank demand deposits suppresses the real rate of interest and will therefore eventually lower the exchange value of the U.S. dollar. The U.S. dollar is currently being propped up by the large volume of foreign participation in the O/N RRP facility.

2021-01-01 11.7

2021-04-01 13.8

2021-07-01 9.0

2021-10-01 14.3

2022-01-01 6.6

2022-04-01 8.5

2022-07-01 7.7

2022-10-01 6.6

2023-01-01 5.1

N-gDp still above target. But there are some ominous signs. What derails economic expansion is a shifting of demand deposits to gated deposits.

Contrary to the myopic banker, from the standpoint of the system, banks create deposits, they do not lend them. This shifting destroys the velocity of circulation (because all bank-held savings originate within the system). I.e., the banks pay for the deposits that they collectively already own. This results in a consolidation of the banks.

Can you hear the sucking sound?

Small-Denomination Time Deposits: Total (WSMTMNS) | FRED | St. Louis Fed (stlouisfed.org)

Large Time Deposits, All Commercial Banks (LTDACBM027NBOG) | FRED | St. Louis Fed (stlouisfed.org)

Call it the paradox of thrift or precautionary savings. But from an accounting perspective, or flow, bank-held savings, stock, are frozen.

See: “Should Commercial banks accept savings deposits?” Conference on Savings and Residential Financing 1961 Proceedings, United States Savings and loan league, Chicago, 1961, 42, 43. By Dr. Leland James Pritchard, Ph.D., Economics, Chicago 1933, M.S. Statistics, Syracuse.

See: “Profit or Loss from Time Deposit Banking”, Banking and Monetary Studies, Comptroller of the Currency, United States Treasury Department, Irwin, 1963, pp. 369-386

re: "Paying interest on the monetary base" Remunerating interbank demand deposits suppresses the real rate of interest and will therefore eventually lower the exchange value of the U.S. dollar. The U.S. dollar is currently being propped up by the large volume of foreign participation in the O/N RRP facility.