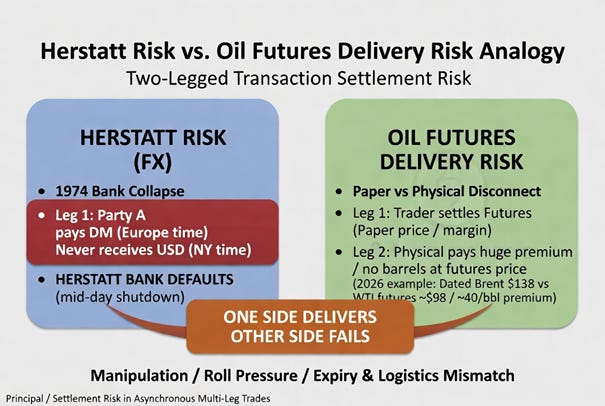

Herstatt Risk

“Everyone imposes his own system as far as his army can reach.” - Joseph Stalin

Watching with interest the latest oil market manipulation with oil prices crashing below $90/barrel, falling by -12% on a report that the United States and Iran were on the verge of a deal to end the conflict, with someone placing a $920 million crude oil short before the publication of the report, making in the process $125 million in profit, when it came to selecting our title analogy, we reminded ourselves of “Herstatt Risk”.

Herstatt Risk (also called FX settlement risk) is a classic example of a two-legged transaction where one party fulfills its obligation but the counterparty fails to deliver the reciprocal legel – often due to timing mismatches across time zones or outright “default”. “Herstat Risk” is named after the 1974 collapse of German Herstatt Bank. In that particular case counterparties had paid Deutsche Marks into the bank’s European accounts, but, when regulators decided to shut the bank down mid-day (before New-York’s USD settlement window), the US Dollars never arrived. One side delivered whereas the other never received. The gap created massive losses and a systemic shock, which it’s why it is a textbook case of principal/settlement risk.

In the current oil markets and its gyrations, the oil futures delivery risk (or more broadly, the physical vs paper large “disconnect”) is we think structurally similar especially in physically deliverable contracts like WTI or Brent near expiry, or in basis trading where you hedge physical oil with futures.

Here is the parallel we are seeing:

Two legs, asynchronous settlement:

· Futures leg (“financial” or “paper”): You settle daily via mark-to-market, post margin, and at expiry the contract either cash-settles or triggers physical delivery at a specific location/quality (e.g., Cushing, Oklahoma for WTI). Most participants never take delivery—they roll or close out.

· Physical leg (“real barrels”): Actual crude loaded onto tankers, stored, or refined, with its own logistics, quality specs, location, and immediate supply/demand realities.

As such, the risk materializes when the two legs fail to converge as expected. You therefore “deliver” on the futures side (or your hedge settles at the screen price), but the physical side doesn’t deliver the matching value - because of storage constraints, transportation bottlenecks, quality mismatches, or (crucially) market manipulations that distort the paper price without reflecting real supply. It’s exactly like in 1974 where the counterparties to Herstatt Bank paid their Deutsche Marks but never received their US Dollars.

In normal times, futures and physical prices stay tightly linked because arbitrageurs enforce convergence near delivery. But when manipulation or exogenous shocks intervene, the gap blows out - just as Herstatt’s time-zone mismatch amplified a counterparty failure.

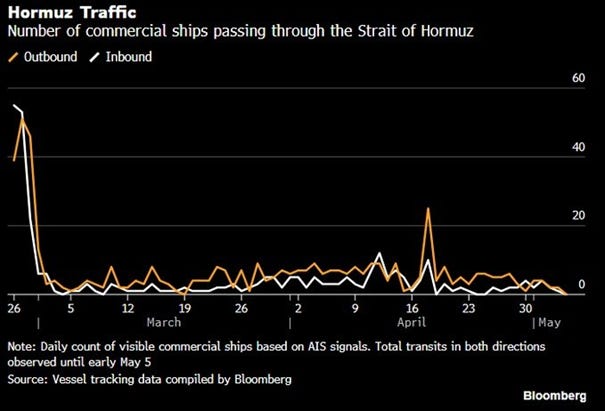

Current (2026) examples make this vivid we think. Geopolitical disruptions (e.g., Strait of Hormuz issues tied to Middle East conflict) have driven physical/spot prices dramatically higher. For instance, we have seen Dubai-linked crude or dated Brent hitting $138–$144/bbl while Brent/WTI futures hovered around $93–$102. Therefore, buyers of real barrels are paying $37–$40+ premiums that futures simply don’t capture. Futures traders (heavy on financial/speculative positioning) are pricing in a quick “peace” resolution and backwardation, while physical buyers face immediate “scarcity”. The paper market has effectively “settled” at one price; the physical market refuses to deliver the expected barrel economics.

Add to this “toxic” mix suspected manipulations such as large, suspiciously timed short positions in futures (hundreds of millions in notional) placed minutes before de-escalation announcements that tanked paper prices like we have seen recently happening and the disconnect becomes even more Herstatt-like. Paper traders can exit or roll without ever touching a barrel; physical players (refiners, producers) are left holding the mismatched exposure. It’s the modern equivalent of sending your currency leg while the counterparty’s leg evaporates due to artificial distortion rather than a bank failure:

- Diagram source Macronomics – Grok generated

The modern twist in oil markets is potentially that the “default” isn’t always a bank failure — it can be paper market manipulation, storage constraints, quality/location basis blowouts, or geopolitical timing that decouples futures from physical reality:

- Graph source Bloomberg – X/Twitter

As such we agree with most of the points made by Amos Hochstein, former Energy Advisor to President Biden on Bloomberg:

“The stock market, the physical market and stock market are divergent at the moment. We may get convergence at some point.”

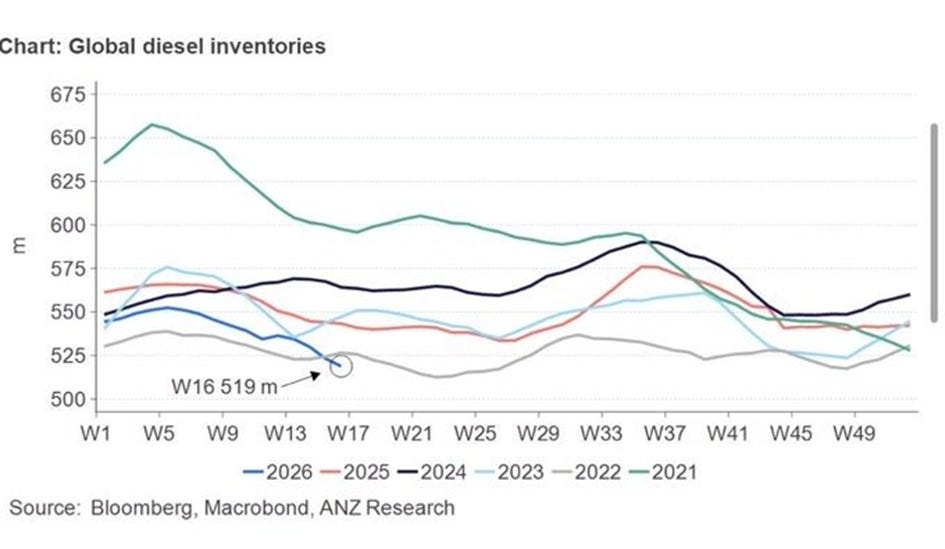

CODIV-19 was all about “demand” destruction, in that case Central Banks had the ability to provide significant “financial support” through “liquidity”. 2026 is a case of “supply shock” and there is very little they can do in the current set up. Meanwhile global diesel inventories are dwindling still as indicated by ANZ:

“Inventory drawdowns do not occur uniformly across the oil complex. They follow a predictable physical sequence, driven by who feels the supply disruption first and which inventory is available/usable at each stage. Given this, we expect product inventories to drawdown first, followed by crude oil and finally strategic stocks. This is already occurring in the diesel market, with global inventories falling below the range seen over the past five years.” – source ANZ

When physical premiums hit $30–$40+/bbl while futures stay “calm,” hedgers are essentially sending their DM leg and praying for the USD leg that never fully arrives:

“The $110 of Brent oil is only available on the Bloomberg terminal” – Amos Hochstein

“Whistling past the graveyard” doesn’t even begin to describe how disconnect from reality the markets seem to us right now but we ramble again…

For those of you interested on our take to the United Kingdom strong exposure to Inflation-linked bonds, here is the link to an article we just published on LinkedIn relating to United Kingdom “convexity risk”.

For those of you interested in “ongoing” Blowbacks and “sovereign credit exposure”, here is the link to an article we just published on LinkedIn relating to Bahrain’s fiscal situation being in the “crosshair”.

In a Pareto efficient economic allocation, “no one can be made better off without at least one individual worse off”.

In this conversation we would like to look at some additional disconnect which has been pointed out as of late such as Chinese TECH (ETF KWEB) relative to US TECH (ETF XLK), why we are keeping our silver exposure as well as touching some several cues from the credit space.

On a side note, we collaborate with friend Geoffrey Fouvry from GraphFinancials as you probably know from reading our Substack Macronomics. As such should you want to subscribe to Geoffrey’s top investing analysis (Geoffrey manages his own portfolio and his performance long/short, no options was around > 150% in 2025) enclosed is a discount link to subscribe to GraphFinancials services of trade recommendations. Geoffrey, like us is old school value but opportunistic as well:

https://buy.stripe.com/4gM6oI2oP7hCfkEbdZ4ZG0m

Also : You can view our most recent YouTube conversation with our friend Zoltan Zselyes CFA, CAIA on our YouTube channel:

The rest of our long monthly musings below with some tactical recommendations (we do also make some good calls) and more in-depth analysis are now for paid subscribers only.

Don’t hesitate to subscribe and share our work if you like our musings or go for a trial.

As well, don’t hesitate to reach out to us if you have any questions or suggestions or want to discuss a specific topic.