Gresham's Law

"Bad money drives out good" - Gresham’s Law

Looking at the ongoing trade wars, with the escalation relating to BRICS and in effect the defense of the US dollar’s reserve status by the Trump administration, as well as the ban of cryptocurrencies by the Chinese authorities, when it came to selecting our title analogy, we reminded ourselves of Gresham’s law. In economics, Gresham’s law is a monetary principle stating that “bad money drives out good”. If there are two coins in circulation containing metal of different value which are accepted by law as having similar face value, the more valuable coin based on the inherent value of its metallic component will gradually disappear from circulation. The law was named in 1857 by economist Henry Dunning Macleod after Sir Thomas Gresham (1519-1579), an English financier during the Tudor dynasty. Gresham at the time had urged Queen Elizabeth to restore confidence in then debased English currency. Beginning of 1971, the US government stopped including any silver in half dollars. The metal value of the 40% silver coins began to exceed their face value which resulted into hoarding. A similar event happened in 2007 with the rising price of copper, zinc, and nickel, which led the U.S. government to ban the melting or mass exportation of one-cent and five-cent coins. In 2025, during the second presidency of Donald Trump, the U.S. Treasury announced a plan to halt penny production starting the following year. The U.S. Treasury will stop minting pennies in early 2026 due to production costs exceeding face value. However, the coin will remain legal tender and in circulation, as only Congress has the power to eliminate forms of currency.

You might be wondering already where we are going with this. We read with great interest on our Linkedin feed the following comment from Alpine Macro Ceo Ritesh Jain:

“There is a great game of power being played.

On one hand president Trump talks about “Bitcoin is the new oil” and on other hand China today has officially banned cryptocurrencies …

US desperately needs Bitcoin and by extension stable coins to succeed because that’s the only way to manage US deficit. As per US treasury secretary, the U.S. treasury bonds demand from stable coins alone will reach $2 trillion by 2030.

On the other hand BRICS currency is GOLD as countries in BRICS are warming up to net settling their trade balances in Gold.

US needs stable coins and bitcoin to succeed… China on the other hand has officially gone on record to ban cryptocurrencies….

The irony is not lost on me…. As China has excess and ample cheap power to mine Bitcoin whereas U.S. will start having blackouts by 2027 due to shortage in power supply.” - Ritesh Jain - Pinetree Macro

Hence our “Gresham’s law” title analogy. In addition to being melted down for its bullion value, money that is considered to be "good" tends to leave an economy through “international trade” (gold is flying East…). International traders are not bound by legal tender laws as citizens of the issuing country are, so they will offer higher value for “good coins” than “bad ones”. The “good coins” may leave their country of origin to become part of international trade, escaping that country's legal tender laws and leaving the "bad" money behind. It happened before. This occurred in Great Britain during the period of adoption of the gold standard: In 1717 Isaac Newton, then Master of the Mint, declared the gold guinea to be worth 21 silver shillings. This overvalued the gold guinea in Great Britain, making it "bad", and encouraged people to send "good" silver shillings abroad, where it could buy more gold than at home. This gold was then minted as currency, which bought silver shillings, which were sent abroad for gold, and so on. For a century hardly any silver coins were minted in Great Britain, and Britain moved onto a de facto gold standard.

As we pointed out in our last musing entitled “Yumin Zhengce”, we contended that the more financialized an economy is, the more “unstable” it becomes. As such, one could argue that the primary mandate of the US Fed has switched from “price stability” to “asset prices” stability.

In March 2025, the S&P 500 lost approximately $5 trillion in market value over three weeks, dropping from a peak of $52.06 trillion to $46.78 trillion, driven by fears of a trade war and economic slowdown. This correction saw the index decline by over 10% from its February 19 high. Earlier, in April 2025, another sharp sell-off wiped out $5 trillion over two days, with a single-day loss of $2.4 trillion on April 3, marking the largest one-day drop since March 2020. These declines were followed by partial recoveries, as by July 25, 2025, the S&P 500 had gained more than 28% from its April 7 low, with periods of record highs, indicating significant bounces in market value. This is what we mean when we argue that the more financialized the US economy is, the more “unstable” is its stock market becomes. Add to this high degree of concentration with the magnificent 7 in the Tech space responsible for the large swings we are seeing.

The S&P 500 dropped 2.36% (approximately $1.2 trillion) due to a weak Nonfarm Payrolls report and new tariff impositions on Friday. This was followed by a partial recovery, as S&P 500 futures rose over 0.5% on August 4 before the market opened, signaling a potential bounce driven by dip-buying and strong premarket action from stocks like Amazon and Nvidia.

In continuation to the points we made relating to the “Turkish solution” which was as well discussed in April 2024 in our conversation “Structured crtiticality, we would like to recommend the video made by Infranomics on Youtube on the 3rd of August entitled “Trump Goes Emerging Market – What does an EM Crisis Look Like”:

“Imagine a country where political pressure overrides economic logic—where central bank independence is eroded, inflation spirals completely out of control, and the currency plummets in value. Sound like a far-off crisis? Think again. This is Turkey’s story, but it’s starting to feel eerily familiar here in the US.” - Infranomics

Obviously, they are some uncanny parallels, particularly with the recent firing of the head of the BLS by president Donald Trump following the significant revisions relating to the Nonfarm payrolls number.

As a reminder, President Recep Tayyip Erdogan fired heads of the Turkish Statistical Institute (TUIK) amid controversies over inflation data. Notably, in January 2022, Erdogan sacked Sait Erdal Dincer, the head of TUIK, after the agency reported a 19-year high inflation rate of 36.1% for December 2021. This move came at a time when opposition parties and independent researchers, like the Inflation Research Group (ENAG), challenged TUIK’s figures, claiming actual inflation was significantly higher (e.g., ENAG estimated 82.81% for December 2021). No official reason was given for Dincer’s dismissal, but critics suggested it was due to Erdogan’s dissatisfaction with the reported numbers, which he reportedly felt overstated Turkey’s economic issues. Since 2018, TUIK has seen multiple leadership changes, with five heads replaced, fueling concerns about its independence. These actions align with Erdogan’s broader economic interventions, including his unorthodox policy of lowering interest rates despite soaring inflation, which he argues helps control prices, contrary to mainstream economic theory.

Turkish President Recep Tayyip Erdogan has also a history of replacing and criticizing central bank governors, particularly over disagreements on monetary policy, especially interest rates, which he believes should be kept low to stimulate the economy, contrary to mainstream economic theory.

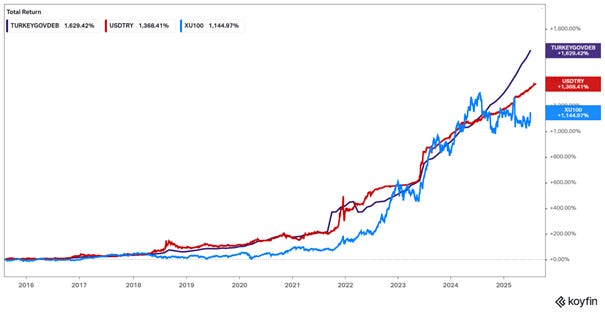

In the case of Turkiye, below is a chart displaying the rise of the Turkish government debt, the depreciation of the currency (USD/TRY) and the significant rise of the Turkish stock market:

- Graph source Macronomics – KOYFIN

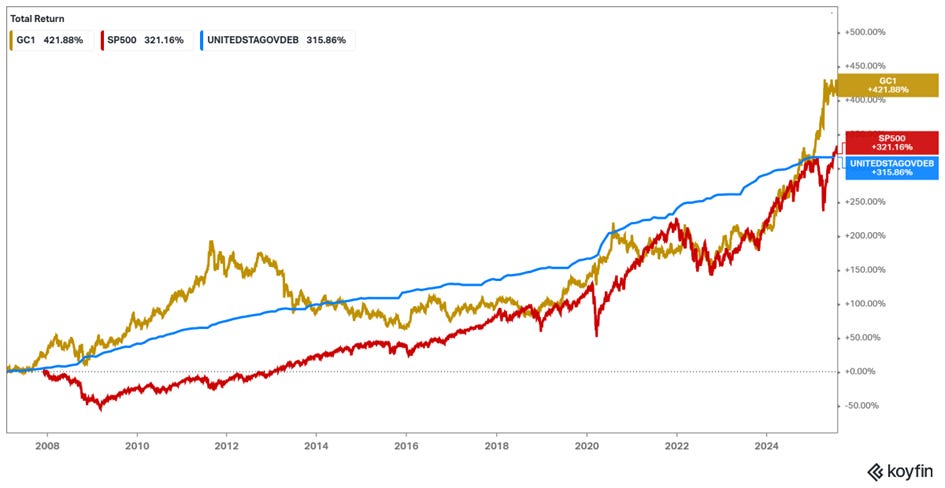

In the below chart we have plotted Gold, S&P500 and United States Government Debt since January 2007:

- Graph source Macronomics – KOYFIN

The Compounded Annual Growth Rate (CAGR) for both the US Government Debt and the S&P500 has been around 8% from the period of 2007 until today.

To re-iterate what we pointed out in our previous conversation, it appears clear to us that the United States is heading towards “Fiscal Dominance” à la Turkiye.

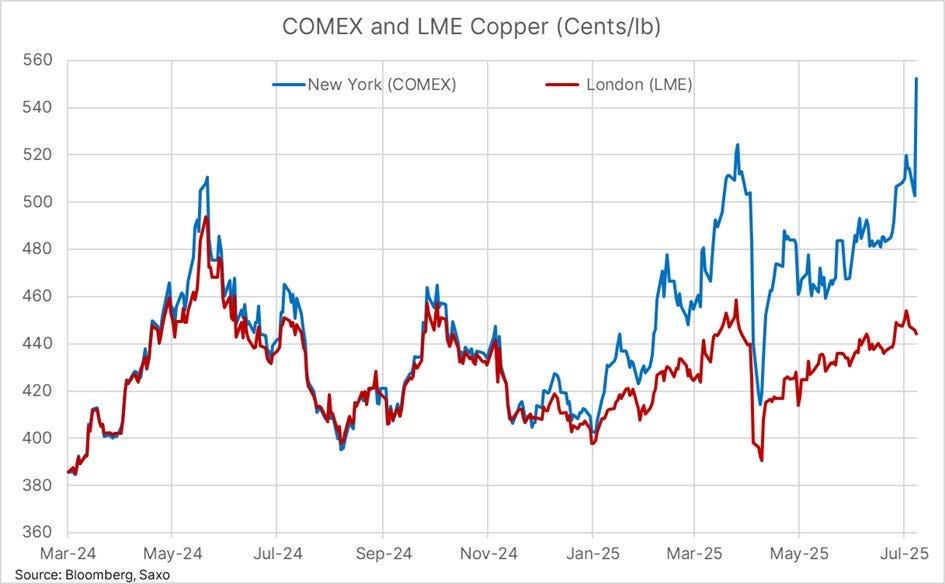

On a side note, in our last conversation we indicated that Olse S. Hansen from Saxo bank highlighted the premium paid for front month copper futures in New-York standing now 25% above 3 month London benchmark:

- Graph source Ole S. Hansen – Saxo Bank – Bloomberg

To quote Stefan Zweig:

"Every wave, regardless of how high and forceful it crests, must eventually collapse within itself." - Stefan Zweig (1881-1942)

No wonder that this “abnormal premium” did not remain as such:

"HG copper trades at a small premium to the LME, but with CME-monitored stocks at a 21-year high—thanks to tariff arbitrage— there is short-term risk of it falling below in order to entice demand from overseas buyers." - Ole S Hansen - Saxo

In the copper case, obviously, some financial pundits got taken to the woodshed as indicated by Bloomberg in their article “Goldman Told Clients to Go Long Copper a Day Before Price Plunge”:

"Goldman suggested clients buy September calls with a $6.25 strike price – about 11% above the prevailing price at the time. Since the tariff announcement and resulting price collapse, the value of those options has plunged by more than 90%." – Bloomberg

No guess on who was on the other side of the trade...Plus ça change as we say in French.

But returning to our “Money illusion” theme and “Fiscal Dominance” à la Emerging Markets, in Turkish style, Turkiye’s debt as a percentage of GDP accounted to 25.6% of the country’s nominal GDP in September 2024, the data reached an all-time high of 75.5% in December 2001 and is now at a record low. This is what we said in our last post:

“If indeed the objective is similar to Turkiye, namely to “destroy” the currency in order to reduce the debt to GDP, then indeed the massive tax on consumers is a sure way of achieving the weakening of the currency while boosting the stock market in the process.” – Macronomics, July 2025

We do see uncanny similarities between the Turkish experience with the current set up and populism drift in the United States.

In this conversation we would like to look at the weaker signs we are starting seeing coming from credit markets, which in our opinion are too complacent relative to the macro weakening backdrop. As well we continue to view positively exposure to the Chinese markets from a valuation perspective. We are not falling for the “jedi tricks” telling us that China is “uninvestable” in Ed Yardeni fashion. Performance YTD speaks for itself.

The rest of our long monthly musings below with some tactical recommendations and more in-depth analysis are now for paid subscribers only.

Don’t hesitate to subscribe and share our work if you like our musings or go for a trial.

As well, don’t hesitate to reach out to us if you have any questions or suggestions or want to discuss a specific topic.