Croesus

“No one is so foolish as to prefer to peace, war, in which, instead of sons burying their fathers, fathers bury their sons.” - Croesus

Watching with interest the euphoria or Fear Of Missing Out (FOMO) crowd pile onto the SpaceX IPO, making Elon Musk, on paper the wealthiest individual of the planet, reaching the dizzying status of “trillionaire”, when it came to selecting our analogy given our continuous fondness for ancient history, we decided to go for “Croesus”. Croesus in ancient history was the last king of Lydia from 585 or 561 BC to 547 BC. Not only was he renowned for his great wealth, he was also known for his ultimate defeat by the Persian king Cyrus the Great following the siege of Sardis. Croesus hoped to quell the growing power of Achaemid Persia and was hoping to expand his own dominions. Croesus thought himself certain of success since he was deluded by the ambiguous assurances of the apparently-reliable oracle of Apollo at Delphi. Although initially Croesus was defeated by Cyrus at the Battle of Thymbra, Croesus decided to “double down” and he was still confident of his chances because he had sent for immediate aid from Sparta, the strongest state in Greece and his firm ally, and hoped to enlist the Egyptians, the Babylonians and others in his coalition against Persia as well. Unfortunately for Croesus, the Spartans were then occupied in a war with neighboring Argos, and neither they nor any other of Croesus’s allies would assemble in time. Sardis was a well-fortified city consecrated by ancient prophecies to never be captured, but, Cyrus intervened and inflicted a series of defeats on Croesus before capturing the capital Sardis, bringing the Lydian kingdom to an end.

In Greek and Persian cultures the name of Croesus became a synonym for a wealthy man. Croesus’ wealth remained proverbial beyond classical antiquity: in English as well as in French, expressions such as “rich as Croesus” or “richer than Croesus” are used to indicate great wealth to this day. The Greek sage Solon was shown by Croesus his immense wealth and was asked who the happiest man in the world was. Solon went to explain that Croesus could not be the happiest man in the world because the fickleness of fortune means that the happiness of a man’s life cannot be judged until after his death.

On a side note, Croesus is credited with issuing the first true gold coins with a standardized purity for general circulation, the Croeseid (following on from his father Alyattes who invented minting with electrum coins). After defeating Croesus, Cyrus the Great adopted the use of gold coinage as the main currency of his kingdom. “Croesus and Fate” is also a short story written by Russian writer Leo Tolstoy.

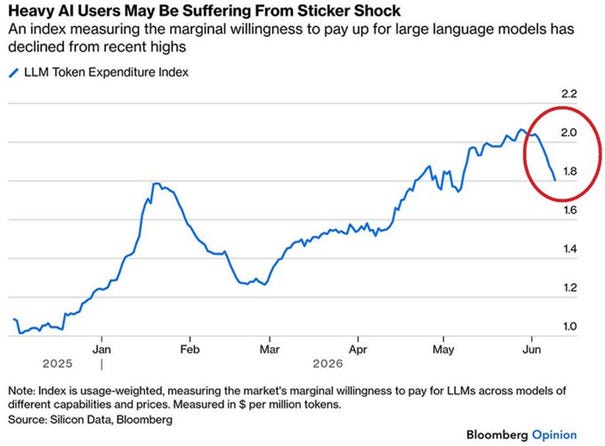

Back in our previous conversation “The Sicilian Expedition”, we argued that the value of “tokens” related to AI would have to “depreciate” and as such at some point lofty “valuations” would have to be re-assessed in the lofty Hyperscaler AI space:

- Graph source Bloomberg – X/Twitter

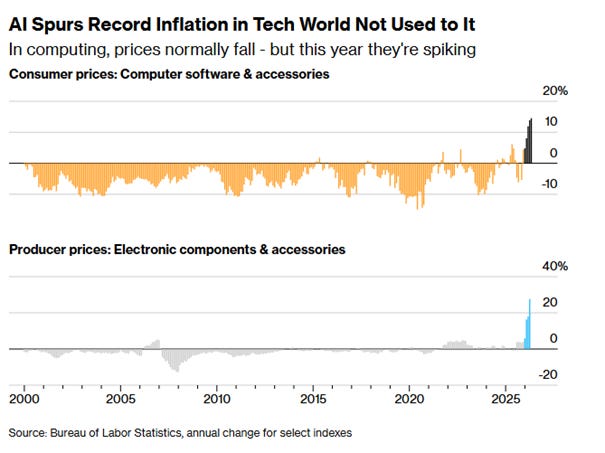

On top of pressure on “token” prices there are rising costs involved:

“Headline inflation climbed back above 4% last month for the first time since the spring of 2023. While the principal cause is an oil spike, triggered by the US war in Iran, AI is chipping in too.” - Bloomberg

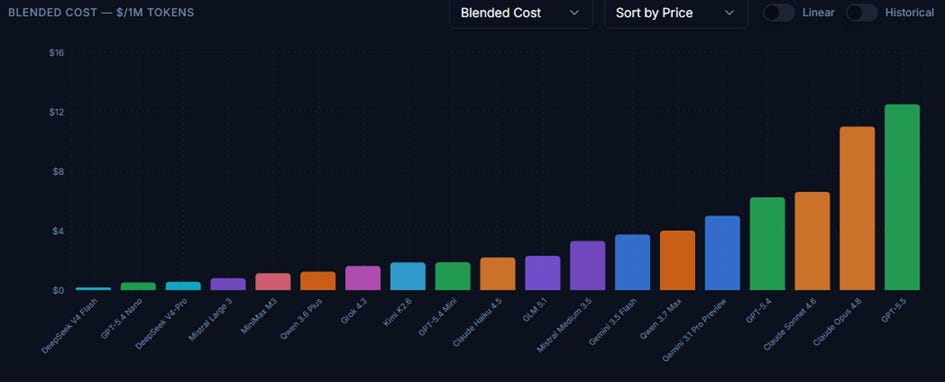

Not only are we seeing cost deterioration, but we are seeing as well price deterioration with DeepSeek, NVIDIA model, Kimi (cursor) getting into the market, but also Anthropic and OpenAI constantly decreasing token prices.

On top of that, Chinese competition is heating up and their models are now gaining traction in the US as they are significantly cheaper than US models:

- Graph source – Token Price Index (TPI)

The only way to increase AI adoption is through a price war so all in all “valuations” will have to come down unless the US goes the way of banning Chinese AI.

One can follow the evolution of “token” pricing through the Token Price Index (TPI) website.

As such we were not surprised to see a lot of “defensive” moves when it comes to “strategic” resources/systems:

“The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.” - Anthropic

Protection of “sovereignty” means government are taking more aggressive measures towards software vendors such as Microsoft but not only. Europe is starting to push back on both US/China. This is what we said in our last conversation:

“Sovereignty matters more and more, as such you can expect various regions and countries to follow not only energy/food independence and rare earths sourcing but, as well “independent AI”. This we think is why “scarcity” matters and supply management has been the dominating feature of the success of the Chinese economy in recent years.” – Macronomics, May 2026.

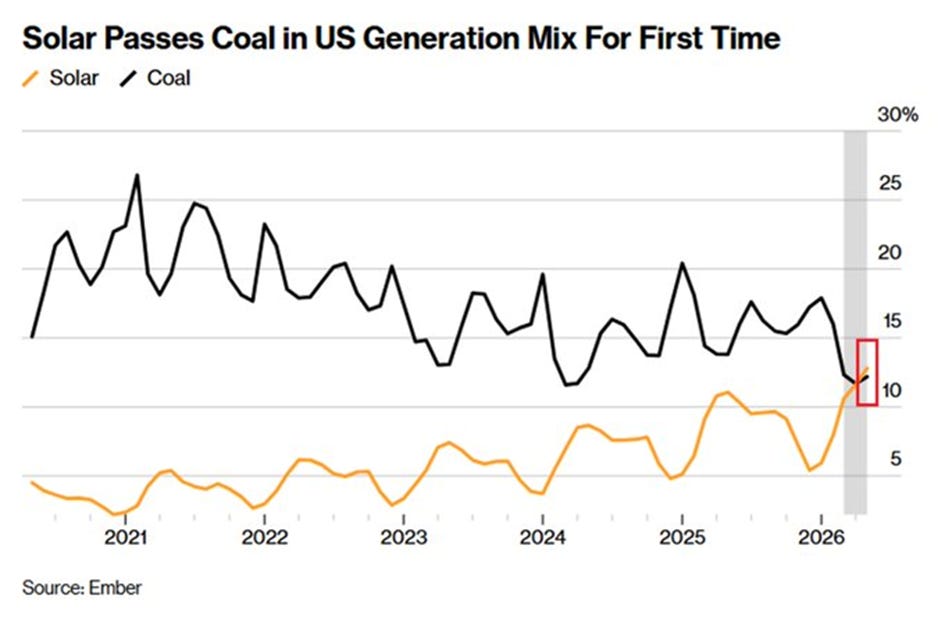

We think the attrition war taking place between China and the United States depends on the cost of energy but funding matters as well. Cheap energy = cheap tokens:

- Graph source Bloomberg – X/Twitter

Solar energy accounted for 12.8% of US electricity production in May, surpassing coal at 12.2%, marking the first time this has occurred in a full calendar month. Solar generation surged +17.0% YoY in May while coal output declined. Though, natural gas remains the dominant source at 37% of the US electricity mix.

Also, one has to take into account the cost of capital, on that side, when one looks at the 10 years Chinese yield, they borrow much cheaper than the United States. As such we have seen rising issuance in Dim Sum bonds as well as the so-called “Panda” bonds by many large corporations. Chinese government borrowing costs remain significantly lower than in the US, driving increased offshore CNY (renminbi) bond issuance, including Dim Sum bonds (CNY-denominated bonds issued and settled outside mainland China, primarily in Hong Kong).

China yields are roughly 2.7–2.8 percentage points (270–280 bp) lower than US yields. This gap has persisted due to China’s accommodative monetary policy, lower inflation/deflationary pressures, and divergence from tighter US rates in prior years. This cost advantage makes CNY funding attractive for issuers who can access it (via swaps or direct use for CNY needs), especially large corporations with operations in China or seeking to hedge/expand in renminbi:

· By early/mid-December 2025: ~CNH 870 billion–1.106 trillion issued (surpassing 2024’s full-year total; eighth consecutive year of expansion). YTD corporate issuance hit records (e.g., ~$46–50 billion equivalent in some reports).

· Strong growth continued into 2026 (e.g., Q1 2026 saw surges of 14–180% YoY in periods, with heavy activity in March).

Tech giants and other multinationals have been prominent, often to fund AI, cloud, overseas expansion, or general operations at lower costs:

· Alibaba: Issued its first major Dim Sum bond in late 2024 — CNH 17 billion (~$2.4 billion).

· Tencent: Debut in 2025 with CNH 9 billion across tranches (e.g., 5/10/15/20/30-year; coupons ~2.1–3.1%), its first bond in four years, tied to AI investments.

· Baidu: Multiple issuances, including CNH 4.4 billion in 2025 (plus earlier activity).

Other sectors (real estate, construction, financials, and global names in energy/mining) are active. Green Dim Sum bonds have also grown.

Panda bond issuance has shown strong growth, with successive records in recent years driven by monetary policy divergence, low Chinese yields, and Beijing’s push to internationalize the RMB.

2026 (YTD as of early June): On track for a new record.

· Q1: Record quarterly high of RMB 88.24 billion (45 deals), up ~101% YoY in volume and 87.5% in deals.

· First 5 months: RMB 136.5 billion, up 90.3% YoY. May alone saw RMB 26.64 billion (record for the month, +246% YoY).

While both Dim Sum Bonds and Panda bonds are RMB-denominated and benefit from lower Chinese rates, Panda bonds are onshore (domestic investors, stricter but deeper market access) vs. Dim Sum (offshore, international investors, more flexibility for some uses). Panda issuance has grown faster recently in relative terms due to onshore liquidity and policy pushes, though Dim Sum remains significant for offshore needs.

Panda bonds (onshore RMB bonds issued by foreign entities in mainland China) generally offer lower yields than Dim Sum bonds (offshore CNH/RMB bonds, primarily in Hong Kong). This reflects deeper domestic liquidity, access to a large pool of onshore Chinese investors, policy support, and tighter integration with the mainland bond market, where benchmark rates are very low.

Panda bonds (onshore): Typically in the 1.7–2.8% range for investment-grade or high-quality foreign issuers, depending on tenor and credit.

Examples:

· Deutsche Bank issued 3-year at 1.72% and 5-year at 1.94% (May/June 2026); earlier March 2026 tranches at 1.95% (3y) and 2.13% (5y). These set records for lowest coupons by foreign issuers.

· Slovenia (sovereign): 3-year at 1.89% (March/April 2026).

· Broader averages: 3-year foreign Panda bonds around 2.15–2.8% in recent periods (2024–2025 data, with 2026 seeing even tighter pricing due to low rates).

· Overall onshore RMB environment: Anchored by China 10-year government bond yield at ~1.74% (June 2026)

Panda bonds often price 20–60+ bp tighter than equivalent Dim Sum for similar issuers/tenors, though the exact gap varies with market conditions.

So not only there is an intensification in the fight over “AI sovereignty” but, as well, cheap energy and cheap funding provide nonetheless the greatest support in the ongoing AI/Token war taking place.

For those of you interested on our take to the United Kingdom strong exposure to Inflation-linked bonds, here is the link to an article we published on LinkedIn in March relating to United Kingdom “convexity risk”.

For those of you interested in “ongoing” Blowbacks and “sovereign credit exposure”, here is the link to an article we just published on LinkedIn relating to Bahrain’s fiscal situation being in the “crosshair”.

In a Pareto efficient economic allocation, “no one can be made better off without at least one individual worse off”.

In this conversation we would like to look at the state of credit markets in general and what the US High Yield CCCs credit canary are telling us. As well, we will like to discuss the current weakness seen in precious metals and miners and what it entails, allocation wise.

On a side note, we collaborate with friend Geoffrey Fouvry from GraphFinancials as you probably know from reading our Substack Macronomics. As such should you want to subscribe to Geoffrey’s top investing analysis (Geoffrey manages his own portfolio and his performance long/short, no options was around > 150% in 2025) enclosed is a discount link to subscribe to GraphFinancials services of trade recommendations. Geoffrey, like us is old school value but opportunistic as well:

https://buy.stripe.com/4gM6oI2oP7hCfkEbdZ4ZG0m

Also : You can view our most recent YouTube conversation with Zoltan Zselyes “The Sicilian Expedition” on our Tube channel:

The rest of our long monthly musings below with some tactical recommendations (we do also make some good calls) and more in-depth analysis are now for paid subscribers only.

Don’t hesitate to subscribe and share our work if you like our musings or go for a trial.

As well, don’t hesitate to reach out to us if you have any questions or suggestions or want to discuss a specific topic.